Chapter 9 Clustering

Until now, we have assumed throughout the book that different units, say \(i\) and \(j\), with \(i\neq j\), never interact in any way. One way we have encoded that is by implicitly assuming that the treatment of individual \(i\) has no impact on the outcomes of individual \(j\). We will clarify this assumption in Chapter 11, and study ways to relax it. Another way we have assumed an absence of interactions is by assuming that all potential outcomes and treatment indicators are independently and identically distributed across observations. We have encoded this restriction at various points, first with Assumption 2.2 in the context of estimating the sampling noise in Randomized Controlled Trials, and then with Assumptions 4.15 and 4.17 in DID settings. This assumption enabled us to leverage the Central Limit Theorem, the most powerful tool we can use to derive asymptotic approximations to our estimators.

The i.i.d. assumption is nevertheless extremely restrictive. It excludes various cases that we are likely to encouter in real life scenarios. For example, this assumption will be wrong if we allocate the treatment at the level of a group of units, such as a village or a firm for example. Groups of units are generally called clusters. In that case, the treatment indicator will not be i.i.d. across observations, since knowing the treatment status of a unit in a given cluster can help us predict the treatment status of its neighbors in the same cluster, so Assumption 2.2 would be violated. The i.i.d. assumption will also be wrong in panel data with repeated observations of the same units if the outcomes are correlated over time for reasons other than having a fixed effect in common. For example, any case in which shocks to outcomes around the fixed effect are somewhat persistent over time, we will have correlation between the observations of the same unit over time, and between the changes in outcomes of the same unit over time. This last issue would violate Assumption 4.15. There are many instances where the shocks to outcomes are likely correlated over time, such as productivity shocks, earnings, education, health, savings, etc, that is most of the outcomes we are generally interested in. Finally, the i.i.d. assumption will also be violated in DID settings in repeated cross sections if the treatment is allocated at a more aggregate level than that of the individual unit. For example, if we study the consequences of laws that vary at the levels of U.S. counties or States, such as minimum wage laws for example, and we have observations on firm’s TFP and employment level, or on individuals’ earnings, then we have correlations between the treatment status of units belonging to the same cluster, and probably the outcomes are correlated as well between the units in the same cluster.

In this chapter, we are going to examine what happens to our traditional estimators when relaxing the i.i.d. assumption, and which new estimators we can use, and what types of diagnostic tests we can make use of in order to assess the severity of the issue. Clustering, as this issue is generally called, has been the topic of a very large literature in econometrics, whose results are sometimes vague, sometimes hard to comprehend or to reconcile, etc. What we are going to do is to try to carve a path through this literature, trying to enlighten its main motivations, its main tools and its main results. We are first going to study the case of clustering in the context of Randomized Controlled Trials. We will then move on to the case of temporal autocorrelation in panel data and we will end with the case of panel data with clustering across time and between observations in each cross section.

9.1 Clustering in Randomized Controlled Trials

What I propose is to first start to see what the problem of clustering does to sampling noise, and how much our default estimator of sampling noise assuming no clustering is biased. I will then introduce the notion of design effect, which is a way to quantify the effect of clustering on sampling noise estimates. Finally, I will propose ways to provide estimates of sampling noise that account for clustering.

9.1.1 An example

Let us first see how that happens in our example before deriving the reason for why we have such a problem and the possible solutions. For that, we are going to simulate data with clusters (such as villages) and we are going to have two features of he data generating process that happen at the cluster level:

- The treatment is going to be randomized at the cluster level. We thus have a clustered randomized controlled trial, where randomization is at the level of clusters regrouping several individual units of observation. For example, think of a classroom where we randomize a new treatment and we observe outcomes at the student level (grades, health status, participation, etc), or think of a cvaccination camoaign randomized at the village level.

- The outcome is going to be autocorrelated within clusters. For example, think of the common determinants of school success (such as the teacher, the parents, the overall conditions at the school) or of the health status in a village (climate, sanitation, pressure by parasites, etc) at the cluster level. These common determinants make the outcomes of two people taken at random in a given cluster more similar than those of two people taken at random in the whole population. The share of the variance in outcomes explained by the variance across clusters is called the intra-cluster correlation coefficient (ICC) and is going to play a key role in what follows.

Example 9.1 Let’s see how we model all of that in our example. We choose to generate the outcomes of individual \(i\) in cluster \(c\) in period \(t\) as follows:

\[\begin{align*} y^0_{i,c,t} & = \mu_{i,c} + U_{i,t} \\ \mu_{i,c} & = \mu^C_c + \mu^U_i \\ U_{i,t} & = \rho U_{i,t-1} + \epsilon_{i,t}, \end{align*}\]

where \(U_{i,0}\), \(\epsilon_{i,t}\), \(\mu^U_i\) and \(\mu_c\) are i.i.d. shocks independent of each other. I introduce a panel data structure because it will be useful for the simulations in the next section.

\(\mu_c\) is the error term varying at the cluster level. We call it a cluster fixed effect. The intra-cluster correlation coefficient is equal to the ratio between the variance in outcomes between clusters and the total variance in outcomes:

\[\begin{align*} ICC_t & = \frac{\sigma^2_{\mu_c}}{\sigma^2_{\mu^c}+\sigma^2_{\mu^U}+\sigma^2_{U_t}}. \end{align*}\]

Let’s generate some data and see what an increase in ICC does to our estimates of the treatment effect in a Brute Force design. As usual, we are going to use the With/Without estimator to compute the treatment effect. Let us first set parameter values:

param <- c(8,.5,.28,1500,0.9,0.01,0.05,0.05,0.05,0.1)

names(param) <- c("barmu","sigma2mu","sigma2U","barY","rho","theta","sigma2epsilon","sigma2eta","delta","baralpha")Let us then simulate one dataset:

N <- 1000

ICC.mu <- 0.2

Nclusters <- 100

set.seed(1234)

# I am going to draw a cluster fixed effect

muC <- rnorm(Nclusters,0,sqrt(param["sigma2mu"]*ICC.mu))

muC <- rep(muC,each=N/Nclusters)

# I draw an individual fixed effect with the remaining variance

muU <- rnorm(N,0,sqrt(param["sigma2mu"]*(1-ICC.mu)))

mu <- param["barmu"] + muC + muU

UBB <- rnorm(N,0,sqrt(param["sigma2U"]))

yBB <- mu + UBB

YBB <- exp(yBB)

epsilonB <- rnorm(N,0,sqrt(param["sigma2epsilon"]))

U0B <- param["rho"]*UBB + epsilonB

y0B <- mu + U0B

epsilonA <- rnorm(N,0,sqrt(param["sigma2epsilon"]))

U0A <- param["rho"]*U0B + epsilonA

y0A <- mu + U0A + param["delta"]

eta<- rnorm(N,0,sqrt(param["sigma2eta"]))

alpha <- param["baralpha"]+ param["theta"]*mu + eta

y1B <- y0B+alpha

y1A <- y0A+alpha

# randomized allocation at the cluster level

Rs <- runif(Nclusters)

# cluster level treatment vector

Rc <- ifelse(Rs<=.5,1,0)

# individual level treatment vector

R <- rep(Rc,each=N/Nclusters)

# outcomes

yB <- y0B

yA <- y1A*R+y0A*(1-R)

# clusters

cluster <- 1:Nclusters

cluster <- rep(cluster,each=N/Nclusters)Let us finally run a set of Monte Carlo simulations, varying ICC:

monte.carlo.BF.ICC <- function(s,N,Nclusters,ICC.mu,param){

set.seed(s)

# I am going to draw a cluster fixed effect

muC <- rnorm(Nclusters,0,sqrt(param["sigma2mu"]*ICC.mu))

muC <- rep(muC,each=N/Nclusters)

# I draw an individual fixed effect with the remaining variance

muU <- rnorm(N,0,sqrt(param["sigma2mu"]*(1-ICC.mu)))

mu <- param["barmu"] + muC + muU

UBB <- rnorm(N,0,sqrt(param["sigma2U"]))

yBB <- mu + UBB

YBB <- exp(yBB)

epsilonB <- rnorm(N,0,sqrt(param["sigma2epsilon"]))

U0B <- param["rho"]*UBB + epsilonB

y0B <- mu + U0B

epsilonA <- rnorm(N,0,sqrt(param["sigma2epsilon"]))

U0A <- param["rho"]*U0B + epsilonA

y0A <- mu + U0A + param["delta"]

eta<- rnorm(N,0,sqrt(param["sigma2eta"]))

alpha <- param["baralpha"]+ param["theta"]*mu + eta

y1B <- y0B+alpha

y1A <- y0A+alpha

# randomized allocation at the cluster level

Rs <- runif(Nclusters)

# cluster level treatment vector

Rc <- ifelse(Rs<=.5,1,0)

# individual level treatment vector

R <- rep(Rc,each=N/Nclusters)

# outcomes

yB <- y0B

yA <- y1A*R+y0A*(1-R)

# regression

ols.ww.BF <- lm(yA ~ R)

ols.ww.BF.yB <- lm(yA ~ R + yB)

# True ICC

data <- as.data.frame(cbind(yB,R))

cluster <- 1:Nclusters

cluster <- rep(cluster,each=N/Nclusters)

data$cluster <- cluster

data <- group_by(data,cluster)

data <- merge(data,summarise(data,yB.mean=mean(yB)))

ICC <- var(data$yB.mean)/var(yB)

return(c(ols.ww.BF$coef[[2]],ols.ww.BF.yB$coef[[2]],ICC))

}

sf.simuls.BF.ICC <- function(ICC.mu,N,Nclusters,Nsim,param){

sfInit(parallel=TRUE,cpus=8)

sfLibrary(dplyr)

sim <- matrix(unlist(sfLapply(1:Nsim,monte.carlo.BF.ICC,N=N,Nclusters=Nclusters,ICC.mu=ICC.mu,param=param)),nrow=Nsim,ncol=3,byrow=TRUE)

sfStop()

colnames(sim) <- c('BF','BF.yB','ICC')

return(sim)

}

Nsim <- 1000

#Nsim <- 50

ICC.val <- c(0,0.05,0.2,0.5,0.8,1)

simuls.BF.ICC <- lapply(ICC.val,sf.simuls.BF.ICC,N=N,Nclusters=Nclusters,Nsim=Nsim,param=param)

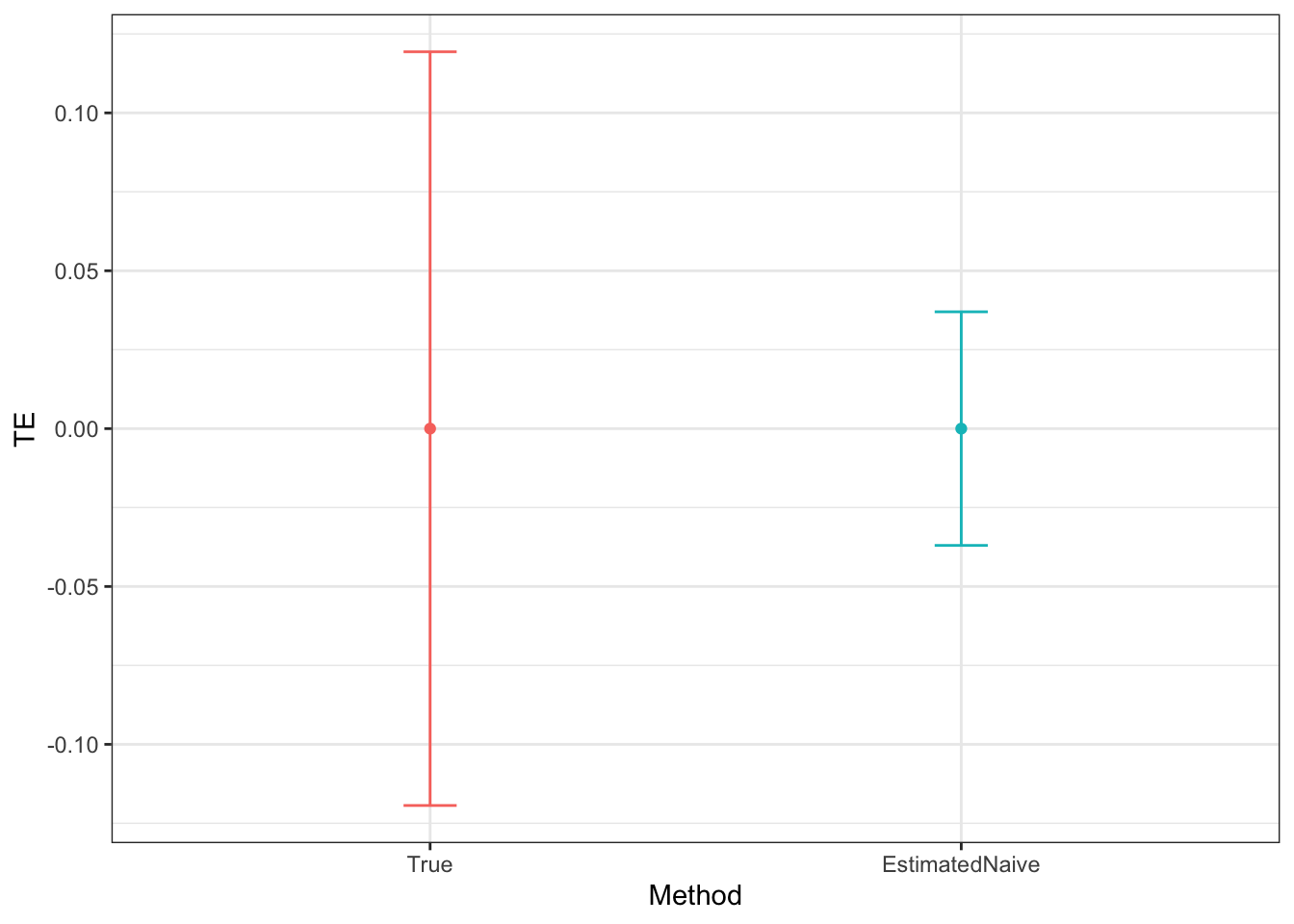

names(simuls.BF.ICC) <- ICC.valLet us now present the results of the simulations:

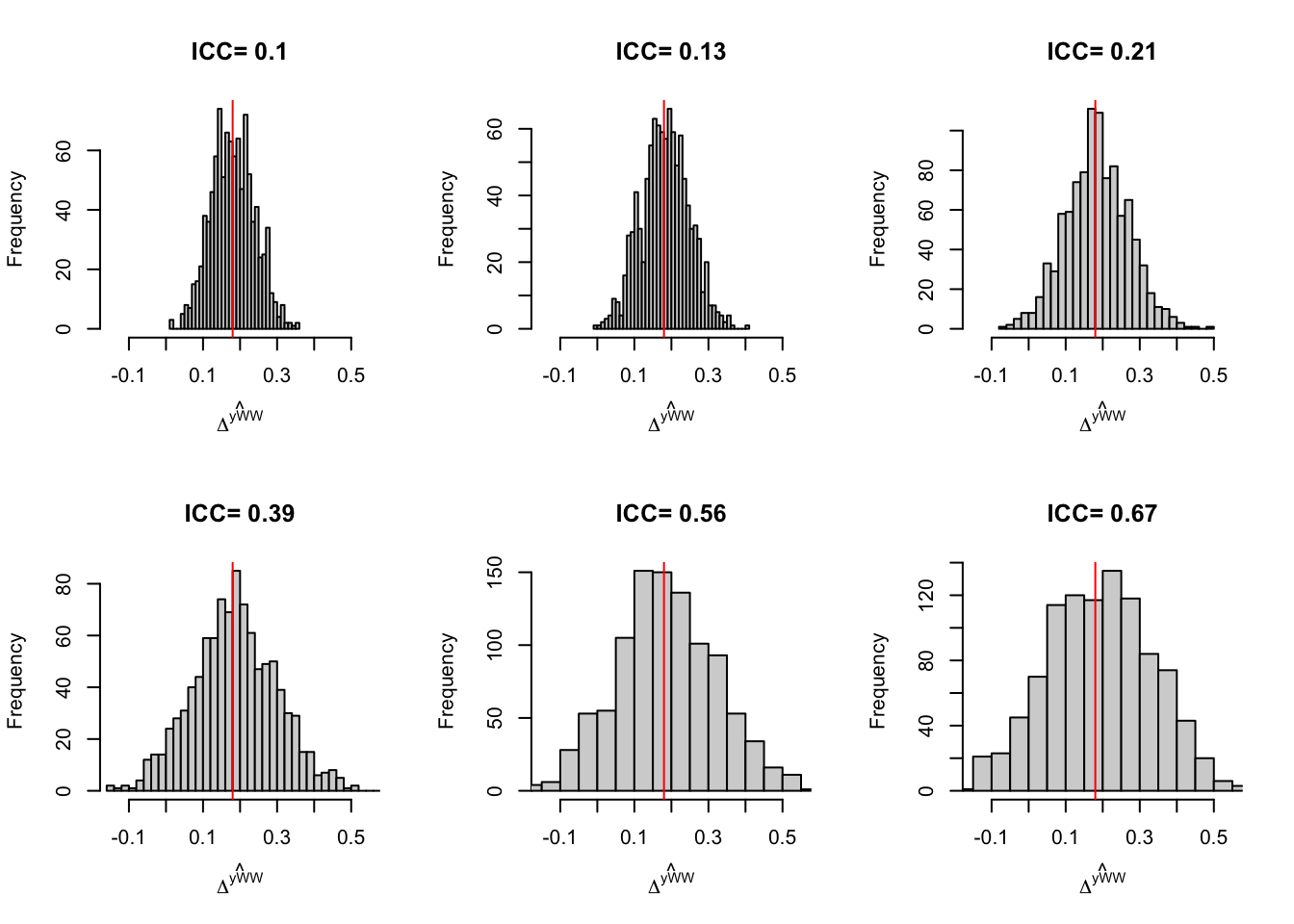

Figure 9.1: Distribution of the \(WW\) estimator in a Brute Force Design for various levels of ICC

Figure 9.1 suggests that increasing the ICC increases sampling noise. Let’s compute sampling noise formally:

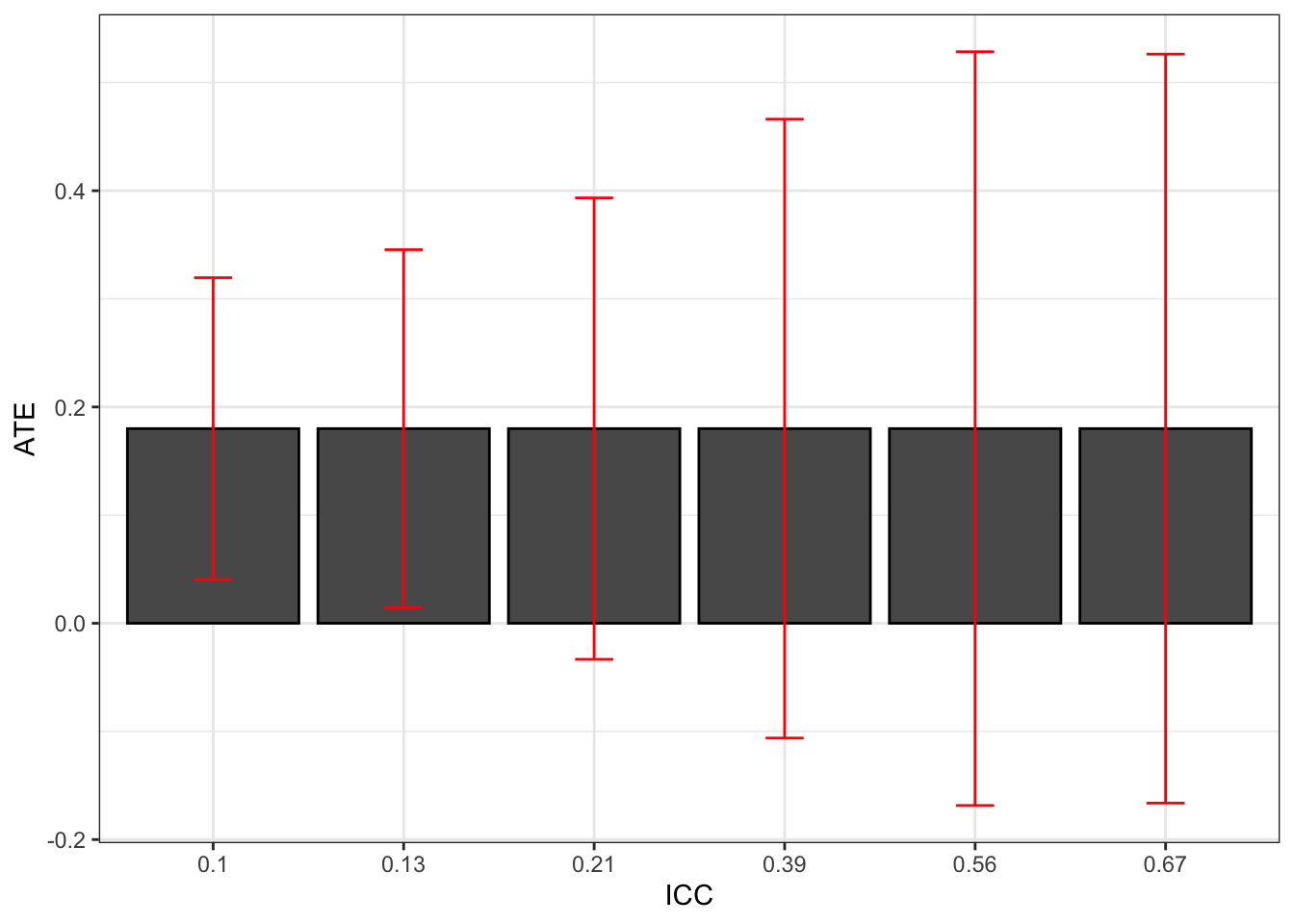

Figure 9.2: Effect of ICC on the 99% sampling noise of the WW estimator in a Brute Force design

Figure 9.2 confirms that increasing the ICC increases sampling noise in a major way. With a small ICC, sampling noise is equal to 0.28, while it is equal to 0.69 with the largest ICC. The difference is more than sizable.

Increasing the ICC is equivalent to losing sample size. The intuition for this result is that, with autocorrelated data, the Central Limit Theorem applies at a much slower pace. The part of the error term that is common to all observations in a given cluster only vanishes as we add more clusters, not as we add more observations per cluster. As a result, this part of sampling noise decreases with the square root of the number of clusters, not with the square root of the number of observations.

The second result to emerge from Figure 9.2 is that ignoring clustering would severely underestimate sampling noise. The lower level of sampling noise on Figure 9.2 is roughly equal to the level of sampling noise that an estimator ignoring clustering would deliver (the estimator detailed in Theorem 2.5). Let’s compute the naive estimator of sampling noise based on Theorem 2.5:

The naive estimate of sampling noise is thus 0.3.

9.1.2 Design effect

A very useful way to understand what clustering does to sampling noise is to derive the variance of the With/Without estimator in the presence of clustering of a simple nature: when all the outcomes within a cluster are correlated in the same way and correlation between outcomes is zero outside of the clusters and all clusters have the same size. This derivation enables us to introduce the notion of design effect, which is a way to quantify the effect of clustering on sampling noise estimates as a function of the ICC. In order to make this derivation, we need to formally specify the covariance matrix of our error terms.

Let us assume that we have access to observations about \(N\) units, allocated in \(n\) clusters of equal size \(m\). Among the \(n\) clusters, \(n_1\) are treated and \(n_0\) are in the control group. Let \(R_{i}\) denote the randomized allocation variable for each unit \(i\), which takes value one when unit \(i\) is located in a cluster \(c\) that has been (randomly) allocated to the treatment and value zero otherwise. Let \(R^C_{c}\) denote the randomized allocation variable for each cluster \(c\), which takes value one when cluster \(c\) has been (randomly) allocated to the treatment and value zero otherwise. Let \(\mathbf{R}_c\) be the vector of randomized allocations at the cluster level: it has length equal to \(n\), and each value is equal to \(R^C_{c}\). Let us denote \(U_i^1=Y_i^1-\esp{Y_i^1|R_{i}=1}\) and \(U_i^0=Y_i^0-\esp{Y_i^0|R_{i}=0}\) and \(U_i=R_{i}U_i^1+(1-R_{i})U_i^0\). Let \(U\) be the vector of all \(U_i\) error terms. Let \(\sigma^2_1=\var{U_i^1}\) and \(\sigma^2_0=\var{U_i^0}\). Finally, let \(\Omega_1\) and \(\Omega_0\) be \(m\times m\) matrices with a diagonal of one and off-diagonal terms all equal to \(\rho_1\) and \(\rho_0\) respectively, with \(\rho_1\) and \(\rho_0\) the Intra-Cluster Correlation Coefficient among the treated and untreated observation respectively. We are now equipped to relax Assumption 2.2:

Hypothesis 9.1 (Clustered Design) We assume that the error terms are clustered:

\[\begin{align*} \esp{UU'} & = \sigma^2_1\diag{\mathbf{R}_c}\otimes\Omega_1+\sigma^2_0(I-\diag{\mathbf{R}_c})\otimes\Omega_0. \end{align*}\]

Remark. Assumption 9.1 imposes that the covariance structure between potential outcomes is block diagonal. That is that there is the same correlation between outcomes for observations in the same cluster, and there is no correlation between outcomes for observations that do not belong to the same cluster.

Theorem 9.1 (Variance of the With/Without estimator under Clustering) Under Assumptions 1.7, 2.1 and 9.1,

\[\begin{align*} \var{{\hat{\Delta^Y_{WW}}}} & = \frac{1}{N}\left(\frac{\sigma^2_0}{1-\Pr(R_i=1)}(1+(m-1)\rho_0)+\frac{\sigma^2_1}{\Pr(R_i=1)}(1+(m-1)\rho_1)\right). \end{align*}\]

Proof. See in Appendix A.5.1.

We can also prove the following corollary:

Corollary 9.1 (Design Effect) Under Assumptions 1.7, 2.1 and 9.1, and with \(\rho_0=\rho_1=\rho\), we have:

\[\begin{align*} \var{{\hat{\Delta^Y_{WW}}}} & = \frac{1}{N}(1+(m-1)\rho)\left(\frac{\sigma^2_0}{1-\Pr(D_i=1)}+\frac{\sigma^2_1}{\Pr(D_i=1)}\right), \end{align*}\]

with \((1+(m-1)\rho)\) the design effect.

Proof. The proof is straightforward using Theorem 9.1.

Remark. Note that the formula for the variance of the \(WW\) estimator in Corollary 9.1 is equal to the formula for the variance of the same estimator under Assumption 2.2 of i.i.d. error terms derived in Lemma A.5 multiplied by the design effect. As soon as \(m>1\), the design effect is strictly superior to one, meaning that the variance of the \(WW\) estimator in a clustered design is superior to the variance of the \(WW\) estimator in a designed where randomization is done at the unit level. The larger the Intra Cluster Correlation Coefficient \(\rho\) and the higehr the number of units per cluster \(m\), the larger the design effect.

Remark. One very useful way to think about the design effect is to think about effective sample size \(N^*=\frac{N}{1+(m-1)\rho}\) as being the sample size that would yield the same precision as our clustered experiment but with an experiment randomized at the unit level. In that sense, the design effect measures by how much clustering decreases our effective sample size.

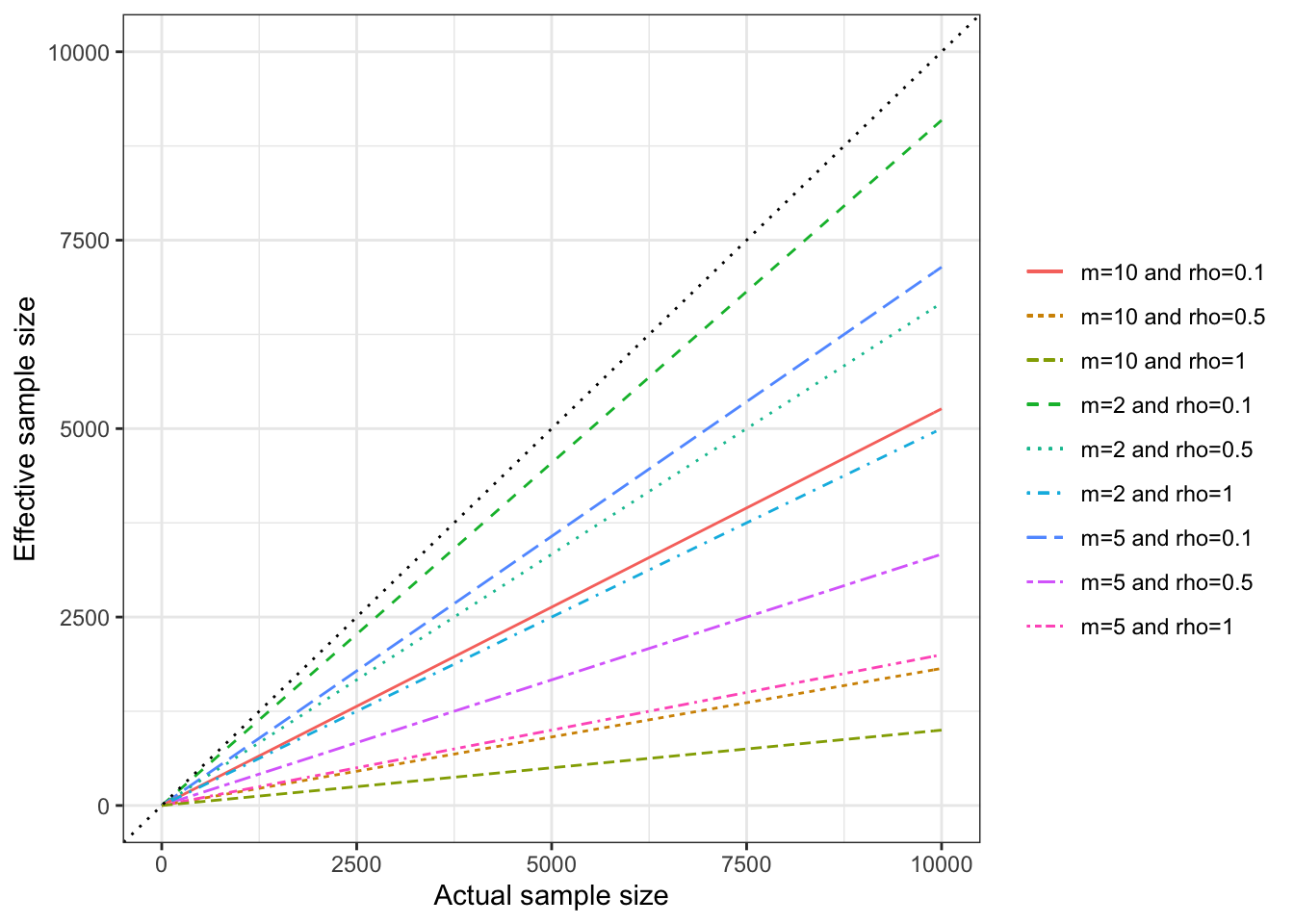

Example 9.2 It is possible to visualize the extent of the design effect is to plot the effective sample size as a function of the real sample size, for various values of \(\rho\) and \(m\). For that, we simply need to generate a function to compute the effective sample size.

DesignEffect <- function(rho,m){

return(1+(m-1)*rho)

}

EffSampleSize <- function(N,...){

return(N/DesignEffect(...))

}Let us now plot the result:

ggplot()+

xlim(0,10000) +

ylim(0,10000) +

geom_function(aes(linetype="m=2 and rho=0.1",color="m=2 and rho=0.1"),fun=EffSampleSize,args=list(rho=0.1,m=2)) +

geom_function(aes(linetype="m=5 and rho=0.1",color="m=5 and rho=0.1"),fun=EffSampleSize,args=list(rho=0.1,m=5)) +

geom_function(aes(linetype="m=10 and rho=0.1",color="m=10 and rho=0.1"),fun=EffSampleSize,args=list(rho=0.1,m=10)) +

geom_function(aes(linetype="m=2 and rho=0.5",color="m=2 and rho=0.5"),fun=EffSampleSize,args=list(rho=0.5,m=2)) +

geom_function(aes(linetype="m=5 and rho=0.5",color="m=5 and rho=0.5"),fun=EffSampleSize,args=list(rho=0.5,m=5)) +

geom_function(aes(linetype="m=10 and rho=0.5",color="m=10 and rho=0.5"),fun=EffSampleSize,args=list(rho=0.5,m=10)) +

geom_function(aes(linetype="m=2 and rho=1",color="m=2 and rho=1"),fun=EffSampleSize,args=list(rho=1,m=2)) +

geom_function(aes(linetype="m=5 and rho=1",color="m=5 and rho=1"),fun=EffSampleSize,args=list(rho=1,m=5)) +

geom_function(aes(linetype="m=10 and rho=1",color="m=10 and rho=1"),fun=EffSampleSize,args=list(rho=1,m=10)) +

geom_abline(slope=1,intercept=0,linetype="dotted",color='black')+

scale_color_discrete(name="") +

scale_linetype_discrete(name="") +

ylab("Effective sample size") +

xlab("Actual sample size") +

theme_bw()

Figure 9.3: Effective sample size in a clustered design

Figure 9.3 shows that effective sample size can decrease enormously because of clustering. For example, with clusters of size \(m=10\), and the Intra Cluster Correlation Coefficient \(\rho=0.5\), a sample size of \(N=10000\) observations is equivalent to an unclustered RCT ran on a sample of \(N^*=\) 1818, which is equivalent to dividing the true sample size by 5.5.

Discuss clustering in the power analysis chapter

9.1.3 Estimating sampling noise accounting for clustering

We have shown that clustering increases sampling noise around our estimates and worse, that our basic estimates of sampling noise based on the i.i.d. assumption underestimate the true amount of sampling noise, sometimes severely. Devising ways to estimate sampling noise that offer a correct estimate of the true extent of sampling noise in the presence of clustering is thus a very important endeavor, if we are to gauge correctly the precision of our treatment effect estimates. Let us see several ways to do that.

Remark. There exists several super cool resources which detail the topics of estimating standard errors under clustering. I really like the one by Cameron and Miller (2015). The one by McKinnon, Nielsen and Webb (2023) is also nice, even if more technical.

9.1.3.1 Using the plug-in formula

One direct and simple way to account for clustering is to use the formula in Theorem 9.1 or the simpler formula in Corollary 9.1. The Intra Cluster Correlation Coefficient can be computed as the ratio of the variance of the mean of the outcomes at the cluster level divided by the total variance of the outcomes in the sample. Once we have an estimate of the variance of the treatment effect, we can build sampling noise \(2\epsilon\) by multiplying the resulting standard error by \(2\Phi^{-1}\left(\frac{\delta+1}{2}\right)\).

Remark. Note that this approach implicitly assumes that the Central Limit Theorem holds with clustered data. Actually, in the clustered case, as long as we allow the number of clusters to go to infinity, we can safely use the classical CLT. We will also see in Section 9.7 that versions of the CLT exist for more general case where there is dependency between data points.

Remark. One uncertainty with the approach relying on CLT based on increasing the number of clusters is that we are unsure whether the normalizing constant in the CLT is \(N\), the total sample size, or \(n\), the number of clusters. This will be rigorously clarified in Sections 9.8 and 9.7.

Example 9.3 In practice, to apply the formula in Theorem 9.1, we simply need to compute the total variance of outcomes in the treated and control groups, and to estimate the Intra Cluster Correlation Coefficients of outcomes among the treated and the controls respectively, \(\rho_1\) and \(\rho_0\). The Intra Cluster Correlation Coefficient can be computed as the ratio of the variance of the mean of the outcomes at the cluster level divided by the total variance of the outcomes in the sample. Let’s go.

# Function for the plug in variance estimator

VarClusterPlugIn <- function(sigma1,sigma0,ICC1,ICC0,p,m,N){

dEffect0 <- 1+(m-1)*ICC0

dEffect1 <- 1+(m-1)*ICC1

return((dEffect0*sigma0/(1-p)+dEffect1*sigma1/p)/N)

}

# Preparing data

dataCluster <- data.frame(Cluster=cluster,yA=yA,yB=yB,R=R)

# Computing ICC

# Cluster-level variance

VaryAClus <- dataCluster %>%

group_by(R,Cluster) %>%

summarize(

MeanyAClus = mean(yA)

) %>%

ungroup(.) %>%

group_by(R) %>%

summarize(

VaryAClus = var(MeanyAClus)

)

# Total variance

VaryA <- dataCluster %>%

group_by(R) %>%

summarize(

VaryATot = var(yA)

)

# ICC

ICC <- VaryA %>%

left_join(VaryAClus,by='R') %>%

mutate(

ICC = VaryAClus/VaryATot

)

# p

p <- mean(dataCluster$R)

# Variance estimate

VarClusteredWW <- VarClusterPlugIn(sigma1=ICC %>% filter(R==1) %>% pull(VaryATot),

sigma0=ICC %>% filter(R==0) %>% pull(VaryATot),

ICC1=ICC %>% filter(R==1) %>% pull(ICC),

ICC0=ICC %>% filter(R==0) %>% pull(ICC),

p=p,

m=N/Nclusters,

N=N)Our estimate of sampling noise accounting for clustering using the plug-in estimator is equal to 0.53. The true level of sampling noise estimated from the simulations is 0.43. Remember that the naive estimate of sampling noise which ignores clustering is 0.3.

9.1.3.2 Using cluster-robust standard errors

The most widely used approach for accounting for clustering when estimating treatment effects is using cluster-robust standard errors. We start with the formula for the variance of the OLS estimator, that we have derived in the proof of Theorem 9.1: \(\var{\hat{\Theta}_{OLS}|X}=(X'X)^{-1}X'\esp{UU'|X}X(X'X)^{-1}\). The basic idea of clustered robust standard errors is to build an empirical estimate of the covariance matrix of the residuals \(\esp{UU'|X}\) using the estimated residuals \(\hat{U}_i\). We might want to use the full \(\mathbf{\hat{U}}\mathbf{\hat{U}}'\) matrix, with \(\mathbf{\hat{U}}\) the vector of all estimated residuals, but that would not work, because, by construction, the OLS estimator produces residuals which are orthogonal to the covariates, so that \(X'\esp{UU'|X}X\) is a null matrix.

Instead, cluster-robust standard errors are estimated by assuming first that the matrix \(\esp{UU'|X}\) is block diagonal, meaning that observations are only correlated within clusters. Let \(\mathbf{\hat{U}}_c\) be the vector of empirical residuals of observations residing in cluster \(c\). Let’s write \(\hat{\Omega}_c=\mathbf{\hat{U}}_c\mathbf{\hat{U}}_c'\) and \(\hat{\Omega}=\diag(\left\{\hat{\Omega}_c\right\}_{c=1}^n)\). We can now use \(\hatvar{\hat{\Theta}_{OLS,Clustered}}=(X'X)^{-1}X'\hat{\Omega}X(X'X)^{-1}\) as our cluster-robust estimate of the covariance matrix of the OLS estimator, with \(\Theta=(\alpha,\beta)\) the parameter vector in the equation \(Y_i=\alpha+\beta R_i+U_i\), where \(\beta=\Delta^Y_{WW}\), as Lemma A.3 shows.

In practice, some authors and statistical software might add a degrees of freedom correction to these estimates as a way to curb small sample bias. One common correction factor is \(\frac{n}{n-1}\frac{N-1}{N-k}\) with \(K\) the number of covariates. Another classical correction is \(\frac{n}{n-1}\).

Example 9.4 Let’s see how these approaches work in our example.

The most straightforward way to implement the cluster-robust variance estimator in R is to use the vcovCL command from the sandwich package.

The type option of vcovCL can take values HC0, where the only correction is \(\frac{n}{n-1}\), and HC1, where the correction is \(\frac{n}{n-1}\frac{N-1}{N-k}\).

Another approach is to use the feols function of the fixest package with the cluster option.

# regression

RegBFCLuster <- lm(yA ~ R, data=dataCluster)

# cluster-robust standard error

VCovClusterHC1 <- vcovCL(RegBFCLuster,cluster=~cluster,type="HC1",sandwich=TRUE)

VCovClusterHC0 <- vcovCL(RegBFCLuster,cluster=~cluster,type="HC0",sandwich=TRUE)

# using fixest

RegBFCLusterFixest <- feols(yA ~ R | 1, data=dataCluster, cluster="Cluster")With the HC1 correction, our estimate of sampling noise accounting for clustering using the plug-in estimator is equal to 0.46, and to 0.46 with the HC0 correction and to 0.46 with fixest.

The true level of sampling noise estimated from the simulations is 0.43.

Remember that the naive estimate of sampling noise which ignores clustering is 0.3.

9.1.3.3 Using Feasible Generalized Least Squares

As Cameron and Miller (2015) remark, when error terms are autocorrelated, the OLS estimator is not the most efficient one, and a Generalized Least Squares (GLS) estimator could perform better. The problem is to find the Feasible Generalized Least Squares estimator that makes real this potential gain in precision. In order to derive it, we have first to specify a model for \(\Omega_{GLS}=\esp{UU'|X}\). One such model is the one in Assumption 9.1. Under such a model, we know that the GLS estimator of the parameter vector \(\Theta=(\alpha,\beta)\) in the equation \(Y_i=\alpha+\beta R_i+U_i\) is \(\hat{\Theta}_{GLS}=(X'\Omega_{GLS}^{-1}X)^{-1}X'\Omega_{GLS}^{-1}Y\). With a consistent estimator for \(\Omega\), e.g. \(\hat{\Omega}_{FGLS}\), we have \(\hat{\Theta}_{FGLS}=(X'\hat{\Omega}_{FGLS}^{-1}X)^{-1}X'\hat{\Omega}_{FGLS}^{-1}Y\) with the associated estimated variance: \(\hatvar{\hat{\Theta}_{FGLS}}=(X'\hat{\Omega}_{FGLS}^{-1}X)^{-1}\). Cameron and Miller (2015) also suggest that we can build a cluster robust estimate of the variance of the FGLS estimator as follows: \(\hatvar{\hat{\Theta}_{FGLS,Clustered}}=(X'\hat{\Omega}_{FGLS}^{-1}X)^{-1}X'\hat{\Omega}_{FGLS}^{-1}\hat{\Omega}\hat{\Omega}_{FGLS}^{-1}X(X'\hat{\Omega}_{FGLS}^{-1}X)^{-1}\), with \(\hat{\Omega}=\diag(\left\{\hat{\Omega}_c\right\}_{c=1}^n)\), \(\hat{\Omega}_c=\mathbf{\hat{U}}_c\mathbf{\hat{U}}_c'\) and \(\mathbf{\hat{U}}_c\) be the vector of empirical residuals of observations residing in cluster \(c\), as in the previous section, but obtained with the FGLS model now.

Remark. As Cameron and Miller (2015) remark, the approach of building a cluster-robust estimator for the variance of the FGLS estimator has been popularized in biostatistics by Liang and Zeger (1986).

Example 9.5 Let’s see how the FGLS approach works in our example. Following Assumption 9.1, we know that \(\hat{\Omega}_{FGLS}=\hat{\sigma}^2_1\diag{\mathbf{R}_c}\otimes\hat{\Omega}_1+\hat{\sigma}^2_0(I-\diag{\mathbf{R}_c})\otimes\hat{\Omega}_0\), with \(\hat{\sigma}^2_1\) the estimated variance of outcomes in the treated group, \(\hat{\sigma}^2_0\), the estimated varianc of outcomes in the control group and \(\hat{\Omega}_1\) and \(\hat{\Omega}_0\) matrices with a diagonal of one and off-diagonal elements equal to \(\hat{\rho}_1\) and \(\hat{\rho}_0\), respectively, the Intra Cluster Correlation Coefficient of outcomes in the treated and untreated groups respectively. We know how to estimate all these parameters so we can build \(\hat{\Omega}_{FGLS}\). Let’s do it.

# Omega matrix at the cluster level

Omega1 <- matrix(data=ICC %>% filter(R==1) %>% pull(ICC),nrow=N/Nclusters,ncol=N/Nclusters) + diag(1-ICC %>% filter(R==1) %>% pull(ICC),nrow=N/Nclusters,ncol=N/Nclusters)

Omega0 <- matrix(data=ICC %>% filter(R==0) %>% pull(ICC),nrow=N/Nclusters,ncol=N/Nclusters) + diag(1-ICC %>% filter(R==0) %>% pull(ICC),nrow=N/Nclusters,ncol=N/Nclusters)

# sigma1 and sigma0

sigma21 <- ICC %>% filter(R==1) %>% pull(VaryATot)

sigma20 <- ICC %>% filter(R==0) %>% pull(VaryATot)

# OmegaFGLS matrix at teh sample level

OmegaFGLS <- sigma21*diag(Rc)%x%Omega1 +sigma20*(diag(1,nrow=Nclusters,ncol=Nclusters)-diag(Rc))%x%Omega0

# Inverting Omega

InvOmegaFGLS <- solve(OmegaFGLS)

# matrix of covariates

X <- cbind(1,R)

# FGLS estimator

RegFGLS <- solve((t(X)%*%InvOmegaFGLS%*%X))%*%(t(X)%*%InvOmegaFGLS%*%yA)

# FGLS estimate of WW

WWyFGLS <- RegFGLS[2,1]

# Basic variance estimate of the FGLS estimator

VcovRegFGLS <- solve((t(X)%*%InvOmegaFGLS%*%X))

# estimated basic standard error of WWyFGLS

SeWWyFGLS <- sqrt(VcovRegFGLS[2,2])The FGLS estimator of the treatment effect is equal to 0.24 \(\pm\) 0.2 with \(\delta=0.95\). This means that the basic FGLS estimate of sampling noise is equal to 0.53. The true level of sampling noise estimated from the simulations is 0.43.

Let us now try to estimate the cluster robust variance of the FGLS estimator.

This requires to compute the matrix \(\hat{\Omega}_c=\mathbf{\hat{U}}_c\mathbf{\hat{U}}_c'\) for each cluster.

For that, we are going to extract the block diagonal matrix \(\hat{\Omega}=\mathbf{\hat{U}}\mathbf{\hat{U}}'\) using the package diagonal.

# computing FGLS residuals

ResidFGLS <- yA-X%*%RegFGLS

# Product of residuals matrix

HatOmega <- ResidFGLS%*%t(ResidFGLS)

# block diagonal equal to zero

diagonals::fatdiag(HatOmega,size=N/Nclusters) <- 0

# take the UU' matrix and take of the OFF diagonal elements

HatOmega <- ResidFGLS%*%t(ResidFGLS)-HatOmega

# compute the Cluster robust FGLS variance matrix estimator

VcovRegFGLSCluster <- VcovRegFGLS%*%t(X)%*%InvOmegaFGLS%*%HatOmega%*%InvOmegaFGLS%*%X%*%VcovRegFGLS

# estimated clustered standard error of WWyFGLS

SeWWyFGLSCluster <- sqrt(VcovRegFGLSCluster[2,2])This means that the cluster-robust FGLS estimate of sampling noise is equal to 0.46. The true level of sampling noise estimated from the simulations is 0.43.

9.1.3.4 Using the Bootstrap

The bootstrap is a data-intensive non-parametric way to obtain cluster-robust estimates of sampling noise. Here, we are going to use the non-parametric bootstrap, but other bootstrap methods exist. Cameron and Miller (2015) cover some of them.

Remark. A key distinction when we use the bootstrap is whether it can offer asymptotic refinements or not.

The way we implement the non-parametric (or pair) bootstrap is as follows:

- We build a sample of \(N_c\) clusters by sampling with replacement from the original sample,

- For each sample \(b\), we estimate a treatment effect \(\hat{\Delta}^y_{WW}(b)\),

- After computing \(B\) such estimates, we compute the bootstrap-cluster-robust variance estimator as follows:

\[\begin{align*} \hatvar{\hat{\Delta}^y_{WW}}^{Bootstrap}_{Clustered} & = \frac{1}{B-1}\sum_{b=1}^B\left(\hat{\Delta}^y_{WW}(b)-\frac{1}{B}\sum_{b=1}^B\hat{\Delta}^y_{WW}(b)\right)^2. \end{align*}\]

Example 9.6 Let’s see how this works in our example. We first need to generate a dataset with outcomes, treatment and cluster indicators. Then we need to draw repeatedly new vectors of clusters identifiers, with replacement, and compute the WW estimator for each.

# Regroup data and cluster id

# already done in dataCluster

# write a function to draw a new vector of clusters and return the WW estimator

# seed: the seed for the PRNG

# data: the dataset

# cluster: the name of the cluster variable (with cluster variable indexed from 1 to Nc)

# y: the name of the outcome variable

# D: the name of the treatment variable

NPBootCluster <- function(seed,data,cluster,y,D){

# set seed

set.seed(seed)

# compute number of clusters

NClusters <- data %>%

group_by(!!sym(cluster)) %>%

summarize(count=n()) %>%

summarize(NClusters=n())

# draw a sample with replacement

SampleClusters <- data.frame(BootClusters =sample(1:(NClusters[[1]]),size=NClusters[[1]],replace=TRUE)) %>%

left_join(data,by=c('BootClusters'=cluster))

# run regression

RegCluster <- lm(as.formula(paste(y,D,sep='~')),data=SampleClusters)

# WW estimate

WW <- coef(RegCluster)[[2]]

# return

return(WW)

}

# testing

test <- NPBootCluster(seed=1,data=dataCluster,cluster='Cluster',y='yA',D='R')

# programming to run in parallel

sf.NP.Boot.Cluster <- function(Nsim,...){

sfInit(parallel=TRUE,cpus=8)

sfLibrary(dplyr)

sim <- matrix(unlist(sfLapply(1:Nsim,NPBootCluster,data=dataCluster,cluster='Cluster',y='yA',D='R')),nrow=Nsim,ncol=1,byrow=TRUE)

sfStop()

colnames(sim) <- c('WW')

return(sim)

}

# Number of simulations

#Nsim <- 10

Nsim <- 400

# running in parallel

simuls.NP.Boot.Cluster <- sf.NP.Boot.Cluster(Nsim=Nsim,data=dataCluster,cluster='Cluster',y='yA',D='R')## R Version: R version 4.1.1 (2021-08-10)

##

## Library dplyr loaded.The cluster-robust non-parametric bootstrap estimate of sampling noise is equal to 0.48. The true level of sampling noise estimated from the simulations is 0.43.

9.1.3.5 Using Randomization inference

Randomization inference is a different way to obtain estimates of the true level of sampling noise using resampling estimates. One intuitive way of running randomization inference would be to draw new vectors of treatment status at the cluster level and estimate the variability of treatment effect estimates. One problem with that approach is that it does not take into account the fact that treated and control differ by the amount of the treatment effect and that is going to add some additional noise in the estimate. A more rigorous approach follows the suggestion in Imbens and Rubin (2015), Section 5.7 and proceed as follows:

- Assume a size for the treatment effect (let’s call it \(\tau\))

- Compute each potential outcome for each treated (\(\tilde{Y}_i^0=Y_i-\tau\) and \(\tilde{Y}_i^1=Y_i\)) and each untreated (\(\tilde{Y}_i^1=Y_i+\tau\) and \(\tilde{Y}_i^0=Y_i\)) unit in the original sample

- Draw a new treatment allocation \(\tilde{R}^1_i\)

- Compute the realized outcomes \(\tilde{Y}_i=\tilde{Y}_i^1\tilde{R}^1_i+\tilde{Y}_i^0(1-\tilde{R}^1_i)\)

- Compute the \(WW\) estimate \(\tilde{\Delta}^Y_{WW_1}\) using the new treatment allocation \(\tilde{R}^1_i\) and the realized outcomes \(\tilde{Y}_i\)

- Repeat the operation \(\tilde{N}\) times, to obtain \(\left\{\tilde{\Delta}^Y_{WW_k}\right\}_{k=1}^{\tilde{N}}\)

- Compute the empirical p-value \(\tilde{p}(\tau)\) as the proportion of sample draws where \(\left|\tilde{\Delta}^Y_{WW_k}-\tau\right|\leq\left|\hat{\Delta}^Y_{WW}-\tau\right|\), where \(\hat{\Delta}^Y_{WW}\) is the treatment effect estimate in the original sample.

- Repeat for various values of \(\tau\) on a set of points \(\tau_1,\dots,\tau_{K}\).

- Find the values \(\tau^u_{\alpha}\) and \(\tau^l_{\alpha}\) that are such that \(\tilde{p}(\tau^u_{\alpha})\approx\alpha\approx\tilde{p}(\tau^l_{\alpha})\) and \(\tau^l_{\alpha}<\hat{\Delta}^Y_{WW}<\tau^u_{\alpha}\). \(\left[\tau^l_{\alpha},\tau^u_{\alpha}\right]\) is the \(1-\alpha\) cluster robust randomizaiton inference-based confidence interval for \(\hat{\Delta}^Y_{WW}\).

Example 9.7 Let’s see how that works in our example.

# function computing one randomization inference draw for one value of tau

# s: the seed for the PRNG

# data: the dataset

# cluster: the name of the cluster variable (with cluster variable indexed from 1 to Nc)

# y: the name of the outcome variable

# D: the name of the treatment variable

ClusteredRI <- function(s,tau,data,cluster,y,D){

# Compute potential outcomes

data <- data %>%

mutate(

y0 = case_when(

!!sym(D)==1 ~ !!sym(y)-tau,

!!sym(D)==0 ~ !!sym(y),

TRUE ~ 99

),

y1 = case_when(

!!sym(D)==1 ~ !!sym(y),

!!sym(D)==0 ~ !!sym(y)+tau,

TRUE ~ 99

)

)

# drawing alternative treatment vector at cluster level

# compute number of clusters

NClusters <- data %>%

group_by(!!sym(cluster)) %>%

summarize(count=n()) %>%

ungroup(.) %>%

summarize(NClusters=n())

# set seed

set.seed(s)

# randomized allocation at the cluster level

Rs <- runif(NClusters[[1]])

# cluster level treatment vector

Rc <- ifelse(Rs<=.5,1,0)

# dataframe of treated joined to original data

RIdata <- data.frame(ClusterId=1:NClusters[[1]],Rc=Rc) %>%

left_join(data,by=c("ClusterId"=cluster)) %>%

#generating RI observed outcomes

mutate(

yc = y0*(1-Rc)+y1*Rc

)

# estimating the RI WW treatment effect

RegWWRI <- lm(yc~Rc,data=RIdata)

# returning estimate

return(coef(RegWWRI)[[2]])

}

# testing

testRI <- ClusteredRI(s=1,tau=0,data=dataCluster,cluster='Cluster',y='yA',D='R')

# testing sapply

Nsim <- 10

testRIapply <- sapply(1:Nsim,ClusteredRI,tau=0,data=dataCluster,cluster='Cluster',y='yA',D='R')

# parallelize for one value of tau

# programming to run in parallel

sf.RI.Cluster <- function(Nsim,tau,data,cluster,y,D){

sfInit(parallel=TRUE,cpus=8)

sfLibrary(dplyr)

sfExport('dataCluster')

sim <- matrix(unlist(sfLapply(1:Nsim,ClusteredRI,tau=tau,data=data,cluster=cluster,y=y,D=D)),nrow=Nsim,ncol=1,byrow=TRUE)

sfStop()

colnames(sim) <- c('WW')

return(sim)

}

# testing

sf.test.RI <- sf.RI.Cluster(Nsim=Nsim,tau=0,data=dataCluster,cluster='Cluster',y='yA',D='R')

# lapply over values of tau on a grid

# function that takes tau as an input and spits out the empirical p-value

# tau: hypothesized value of treatment effect

# WWhat: estimated vamlue of treatment effect in the original sample

ParallelClusteredRI <- function(tau,WWhat,...){

# computing the RI distribution of WW estimates for given tau

sf.WW.RI <- sf.RI.Cluster(tau=tau,...)

# estimate enpirical cdf of |WWRI-tau|

F.WW.RI.tau <- ecdf(abs(sf.WW.RI-tau))

# Compute the p-value

pvalue <- 1-F.WW.RI.tau(abs(WWhat-tau))

# return the p-value

return(pvalue)

}

# testing

testRItau <- ParallelClusteredRI(tau=0,WWhat=0.2,Nsim=Nsim,data=dataCluster,cluster='Cluster',y='yA',D='R')

# run on a grid of tau's

tau.grid <- seq(from=-0.15,to=0.55,by=0.01)

Nsim <- 1000

simuls.RI.tau <- sapply(tau.grid,ParallelClusteredRI,WWhat=0.2,Nsim=Nsim,data=dataCluster,cluster='Cluster',y='yA',D='R')

names(simuls.RI.tau) <- tau.grid

# putting results in data frame

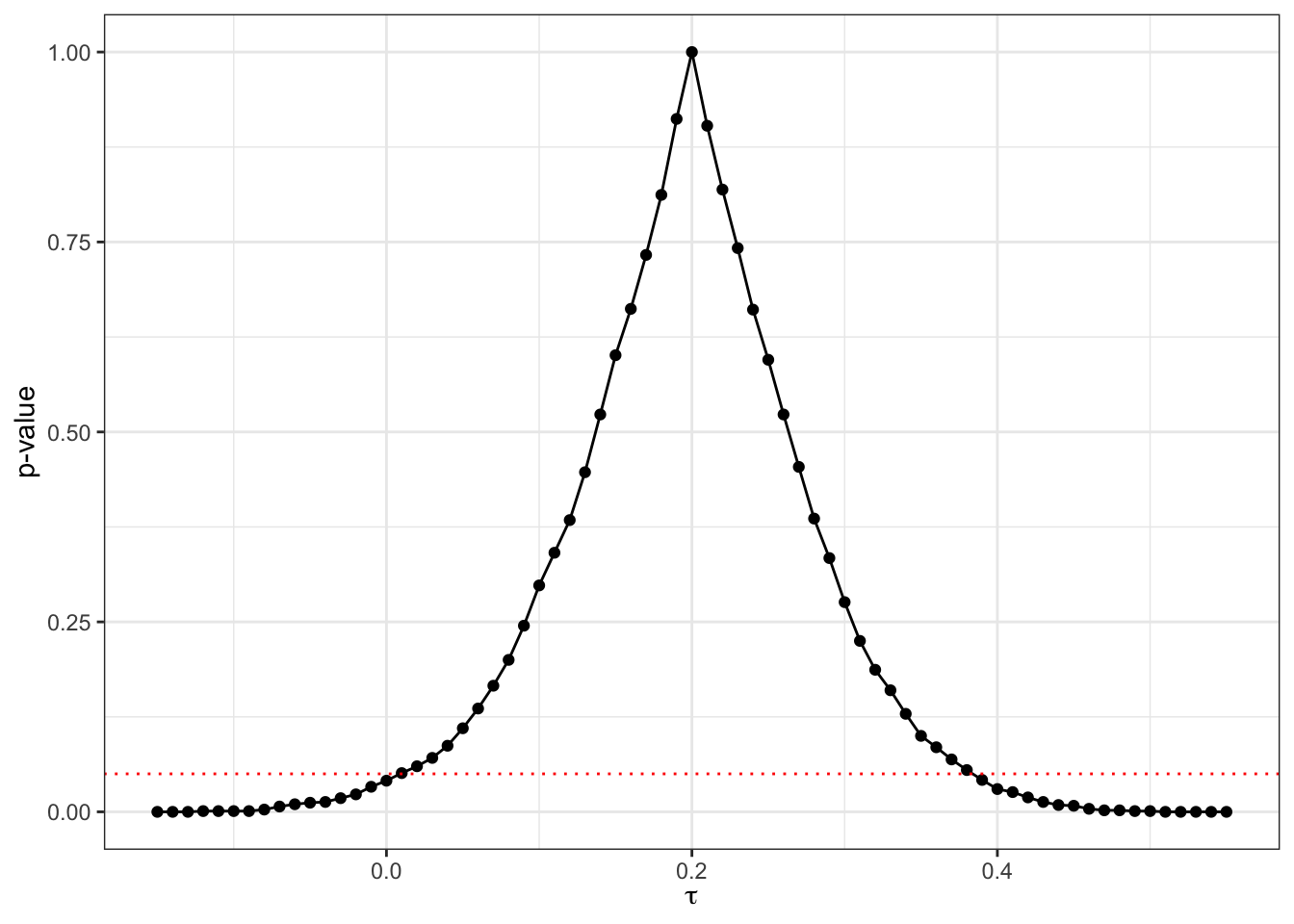

RI.pvalues.tau <- data.frame(pvalue=simuls.RI.tau,tau=tau.grid)Let us visualize the resulting estimates of the p-values as a function of \(\tau\):

ggplot(RI.pvalues.tau,aes(x=tau,y=pvalue))+

geom_point() +

geom_line() +

geom_hline(yintercept = 0.05,linetype='dotted',color='red')+

ylim(0,1) +

ylab("p-value") +

xlab(expression(tau)) +

theme_bw()

Figure 9.4: Randomization inference p-values as a function of \(\tau\)

Let us now compute the confidence interval and estimate of sampling noise:

# computing RI-based confidence interval and sampling noise estimate

# function that takes a dataframe of pvalues and a grid and spits out both ends of confidence interval and level delta and sampling noise

# delta: level of the confidence interval (95% or 99% for example)

# data: a data frame with a variable for tau and a variable for pvalues

# tau: name of the tau variable

# pval: name of the pvalue variable

RI.CI <- function(delta,data,tau,pval){

data <- data %>%

mutate(

# finding observations with pvalue lower than delta

below.pval = case_when(

!!sym(pval) <= 1-delta ~ 1,

!!sym(pval) > 1-delta ~ 0,

TRUE ~99

),

# finding observations below the tau with maximum pvalue

max.pval = max(!!sym(pval)),

max.pval.tau = case_when(

!!sym(pval) == max.pval ~ !!sym(tau),

TRUE ~ -Inf

),

max.pval.tau = max(max.pval.tau),

below.max.paval.tau = case_when(

tau<max.pval.tau ~ 1,

tau>=max.pval.tau ~ 0,

TRUE ~ Inf

)

) %>%

# keeping only observations that are below pval of delta%

filter(below.pval==1) %>%

# grouping by whether tau is above or below the tau with maximum pvalue

group_by(below.max.paval.tau)

# finding max and min values that are extremes of delta% CI

minCI <- data %>%

filter(below.max.paval.tau==1) %>%

ungroup(.) %>%

summarize(

minCI = max(!!sym(tau))

) %>%

pull(minCI)

maxCI <- data %>%

filter(below.max.paval.tau==0) %>%

ungroup(.) %>%

summarize(

maxCI = min(!!sym(tau))

) %>%

pull(maxCI)

# results

results <- list(minCI,maxCI,maxCI-minCI)

names(results) <- c("LowCI","HighCI","SamplingNoise")

return(results)

}

# test

testRICI95 <- RI.CI(delta=0.95,data=RI.pvalues.tau,tau='tau',pval='pvalue')

testRICI99 <- RI.CI(delta=0.99,data=RI.pvalues.tau,tau='tau',pval='pvalue')As a result of our procedure, the randomization inference based 95% confidence interval for the \(WW\) estimator is \(\left[\right.\) 0 , 0.39 \(\left.\right]\) and the 99% sampling noise is equal to 0.5.

The true level of sampling noise estimated from the simulations is 0.43.

Remark. Another, simpler, option for implementing randomization inference would have been simply to reallocate the treatment vector among clusters and keep the original values of the outcomes instead of generating the outcomes under the null for each value of \(\tau\). This is the simple approach we have used in Chapter 2. The properties of this approach have not been studied to my knowledge, but it would be interest!ing to know under which conditions it is approximately correct. Let’s check what would have happened if we had used this simpler approach to randomization inference.

# function computing one simplified randomization inference draw

# s: the seed for the PRNG

# data: the dataset

# cluster: the name of the cluster variable (with cluster variable indexed from 1 to Nc)

# y: the name of the outcome variable

# D: the name of the treatment variable

ClusteredRISimple <- function(s,data,cluster,y){

# drawing alternative treatment vector at cluster level

# compute number of clusters

NClusters <- data %>%

group_by(!!sym(cluster)) %>%

summarize(count=n()) %>%

ungroup(.) %>%

summarize(NClusters=n())

# set seed

set.seed(s)

# randomized allocation at the cluster level

Rs <- runif(NClusters[[1]])

# cluster level treatment vector

Rc <- ifelse(Rs<=.5,1,0)

# dataframe of treated joined to original data

RIdata <- data.frame(ClusterId=1:NClusters[[1]],Rc=Rc) %>%

left_join(data,by=c("ClusterId"=cluster))

# estimating the RI WW treatment effect

RegWWRISimple <- lm(as.formula(paste(y,'Rc',sep='~')),data=RIdata)

# returning estimate

return(coef(RegWWRISimple)[[2]])

}

# testing

testRISimple <- ClusteredRISimple(s=1,data=dataCluster,cluster='Cluster',y='yA')

# testing sapply

Nsim <- 10

testRISimpleapply <- sapply(1:Nsim,ClusteredRISimple,data=dataCluster,cluster='Cluster',y='yA')

# programming to run in parallel

sf.RI.Cluster.Simple <- function(Nsim,data,cluster,y){

sfInit(parallel=TRUE,cpus=8)

sfLibrary(dplyr)

sim <- matrix(unlist(sfLapply(1:Nsim,ClusteredRISimple,data=data,cluster=cluster,y=y)),nrow=Nsim,ncol=1,byrow=TRUE)

sfStop()

colnames(sim) <- c('WW')

return(sim)

}

# testing

sf.test.RI.simple <- sf.RI.Cluster.Simple(Nsim=Nsim,data=dataCluster,cluster='Cluster',y='yA')

# running

Nsim <- 1000

simuls.RI.Simple <- sf.RI.Cluster.Simple(Nsim=Nsim,data=dataCluster,cluster='Cluster',y='yA')

Var.WW.RI.Simple <- var(simuls.RI.Simple)With the simplified randomization inference procedure, the 99% sampling noise is equal to 0.49.

The true level of sampling noise estimated from the simulations is 0.43.

9.2 Clustering in panel data

Another source of clustering appears in panel data, where we follow the same observation over time. One way to account for the correlation between the outcomes of the same individual over time is to add individual level fixed effects, and to use either a within estimator or a Least Squares Dummy Variable estimator, as we did in Section 4.3. But adding individual level fixed effects probably does not account for the overall correlation between observations of the same individual over time. A case in point is autocorrelation in the error terms due to persistent shocks. If a unit has experienced a shock at date \(t\), she is more likely to experience a similar shock at date \(t+1\). For example, health problems do not solve themselves miraculously between survey rounds. In the same manner, job loss or job changes or hurricanes, etc, all have effects that persist over time. As a consequence, we often believe that the observations for the same unit are correlated over time, abve and beyond what can be captured by a unit fixed effect. In this section, we are going to study the issue of clustering in panel data, focusing on the estimators we have studied in Section 4.3, especially the simple DID estimator, the fixed effects estimator, and the Sun and Abraham estimator in staggered designs. A key result of importance is that DID estimates which only involve two-periods are not affected by the autocorrelation problem, while estimates which aggregate more than two periods of data are affected, and the more so as they aggregate more time periods. We are first going to take an example to exemplify the importance of the problem. We will then derive the closed form variance of the various estimators under simplified assumptions on the autocorrelation between error terms. Finally, we will explain how to estimate sampling noise in panel data with autocorrelated error terms.

9.2.1 An example

Let us start with an example of how autocorrelated error terms alter the precision of panel data estimates. For that, we are going to generate long time series of panel data and explore how the variability of treatment effect estimates changes with persistence in error terms at the individual level, both for the event-study estimates (which rely on \(2\times 2\) comparisons) and for the TT estimate, which relies on aggregated treatment effects. For simplicity, we are going to jave a design without staggered entry, but everything we are saying here applies to staggered entry as well.

Check what happens with staggered entry

I am going to use the following model:

We model outcomes dynamics as follows:

\[\begin{align*} Y_{i,t} & = D_{i,t}Y^1_{i,t}+(1-D_{i,t})Y_{i,t}^0\\ Y_{i,t}^1 & = Y_{i,t}^0 + \bar\alpha \\ Y_{i,t}^0 & = \mu_i + U_{i,t} \\ U_{i,t} & = \rho U_{i,t-1} +\epsilon_{i,t} \\ D_{i,t} & = \uns{D^*_{i,k}\geq0}\uns{t\geq k} \\ D^*_{i,k} & = \theta_i + \eta_{i,k}. \end{align*}\]

Outcome dynamics are characterized by an individual fixed effect \(\mu_i\) and an AR(1) process with autoregressive parameter \(\rho\in\left[0,1\right]\). \(\epsilon_{i,t}\) is i.i.d. and has finite variance \(\sigma^2\) and is independent from all the other variables in the model. \(U_{i,0}\) has finite variance \(\sigma^2_{U_0}\) and is independent from all the other variables in the model. The program is only available at period \(k\). Participation in the program (which we denote \(D_{i,t}\)) depends on the utility from entering the program \(D^*_{i,k}\) being positive. \(\eta_{i,k}\) is a random shock uncorrelated with any of the other variables in the model. Selection bias occurs because \(\mu_i\) and \(\theta_i\) are correlated.

Let us now choose some parameter values (but the value of \(\rho\)):

# basic parameter values

param.basic <- c(0.05,0.72,0.55,0.55,0.5,0.1,0)

names(param.basic) <- c("sigma","sigmaU0","sigmamu","sigmatheta","rhosigmamutheta","sigmaeta","baralpha") Note that I have chosen the true effect of the treatment to be zero, which saves me computational difficulties because \(Y_{i,t}=Y^0_{i,t}\), and does not matter at all for now since we are trying to estimate sampling noise and not the treatment effect itself. Let us now encode a function generating one sample for one choice of parameter values and seed and spitting out one estimate of the event study parameters and of the TT parameter based on Sun and Abraham estimator. I am going also to estimate the \(2\times 2\) DID estimator along with its heteroskedasticity robust standard errors, both as a within estimator and as a first-difference estimator, in order to check whether the standard error estimates are similar in all three approaches.

# function generating a sample of outcomes for K time periods with N sample size and spitting out DID estimates (both event study and TT, with both Sunab and )

# seed: seed setting the PRNG

# N: number of units in the panel

# K: number of periods in the panel

# k: treatment date

# param: basic parameters

# rho: value of rho

# cluster: whether we cluster or not our treatment effect estimates for temporal autocorrelation ("None", vs "Temporal")

Outcome.Sample.DID.Long <- function(seed,N,K,k,param,rho,cluster="None"){

# draw all i.i.d. error terms for all years

set.seed(seed)

epsilon <- rnorm(n=K*N,sd=sqrt(param["sigma"]))

# draw initial error term

U0 <- rnorm(n=N,sd=sqrt(param["sigmaU0"]))

# draw fixed effects

sigma.mu.theta <- matrix(c(param["sigmamu"],param["sigmamu"]*param["sigmatheta"]*param["rhosigmamutheta"],

param["sigmamu"]*param["sigmatheta"]*param["rhosigmamutheta"],param["sigmatheta"]

),ncol=2,nrow=2,byrow = T)

mu.theta <- rmvnorm(n=N,mean=c(0,0),sigma=sigma.mu.theta)

mu <- mu.theta[,1]

theta <- mu.theta[,2]

# building dataset (wide format)

data <- as.data.frame(cbind(mu,U0))

for (i in 1:K){

data[paste('U',i,sep="")] <- rho*data[paste('U',i-1,sep="")]+epsilon[((i-1)*N+1):(i*N)]

data[paste('Y',i,sep="")] <- mu + data[paste('U',i,sep="")]

}

# selection rule

# draw error term

data['eta'] <- rnorm(n=N,sd=sqrt(param["sigmaeta"]))

data <- data %>%

mutate(

# generating utility from participation

Ds = theta + eta,

# generating treatment participation

D = case_when(

Ds >0 ~ 1,

TRUE ~ 0

),

# generating treatment identifier for Sun&Abraham estimator with treatment group being at period k

Dsunab = case_when(

D == 1 ~ k,

D == 0 ~ 99,

TRUE ~ -99

)

)

# generate long dataset

data <- data %>%

select(contains("Y"),contains("D")) %>%

mutate(id = 1:nrow(data)) %>%

pivot_longer(starts_with("Y"),names_to = "Period",names_prefix = "Y",values_to = "Y") %>%

mutate(

Period = as.numeric(Period),

TimeToTreatment = case_when(

D == "1" ~ Period-k,

TRUE ~ -99

)

)

# estimating DID model with Sun and Abraham estimator

if (cluster=="None"){

reg.DID.SA <- feols(Y ~ sunab(Dsunab,Period) | id + Period,vcov='HC1',data=data)

}

if (cluster=="Temporal"){

reg.DID.SA <- feols(Y ~ sunab(Dsunab,Period) | id + Period,vcov=cluster~id,data=data)

}

resultsDID.SA <- data.frame(Coef=reg.DID.SA$coefficients,Se=reg.DID.SA$se,Name=names(reg.DID.SA$coefficients)) %>%

mutate(

#TimeToTreatment = as.numeric(str_split_fixed(Name,'::',n=2)[,2])

TimeToTreatment = as.numeric(str_split_fixed(Name,':',n=4)[,3])

) %>%

select(-Name)

# adding reference period

resultsDID.SA <- rbind(resultsDID.SA,c(0,0,-1))

# TT

ATT.SA <- aggregate(reg.DID.SA, c("ATT" = "Period::[^-]"))

ATT.SA <- data.frame(Coef=ATT.SA[[1]],Se=ATT.SA[[2]],TimeToTreatment=99)

# joining results SA

resultsDID.SA <- rbind(resultsDID.SA,ATT.SA)

# estimating DID model with 2x2 FD estimators

tau.FD <- c(-19:-2,0:20)

resultsDID.FD <- map_dfr(tau.FD,StaggeredDID22,y='Y',D='Dsunab',d=20,dprime=99,tauprime=1,t="Period",i="id",data=data) %>%

select(tau,FDEst,FDSe) %>%

rename(TimeToTreatment = tau,

Coef=FDEst,

Se=FDSe) %>%

relocate(TimeToTreatment,.after=Se)

# adding reference period

resultsDID.FD <- rbind(resultsDID.FD,c(0,0,-1))

# adding aggregate ATT

ATT.FD <- resultsDID.FD %>%

filter(TimeToTreatment>=0) %>%

summarize(

ATT = mean(Coef),

# this incorrectly ignores correlations between the FD estimates

SeATT = sqrt(sum(Se^2))/(K-k+1)

) %>%

rename(

Coef = ATT,

Se = SeATT

) %>%

mutate(

TimeToTreatment=99

)

# joining results FD

resultsDID.FD <- rbind(resultsDID.FD,ATT.FD)

# Estimating with Stacked DID FD

if (cluster=="None"){

results.Stacked.DID.FD.Full <- StackedDIDFD(y='Y',D='Dsunab',dprime=99,tauprime=1,t="Period",i="id",data=data)

}

if (cluster=="Temporal"){

results.Stacked.DID.FD.Full <- StackedDIDFD(y='Y',D='Dsunab',dprime=99,tauprime=1,t="Period",i="id",Leung='Temporal',data=data)

}

results.Stacked.DID.FD <- results.Stacked.DID.FD.Full[[1]] %>%

rename(Group=d,

TimeToTreatment = tau,

Coef=TE,

Se=SeTE) %>%

select(-Ddtau)

# adding the ATT

if (cluster=="None"){

ATT.Stacked.DID.FD <- data.frame(Group="All",TimeToTreatment=99,Coef=results.Stacked.DID.FD.Full[["ATT"]],Se=results.Stacked.DID.FD.Full[["ATTSe"]]) %>%

rename(Se=weights)

}

if (cluster=="Temporal"){

ATT.Stacked.DID.FD <- data.frame(Group="All",TimeToTreatment=99,Coef=results.Stacked.DID.FD.Full[["ATT"]],Se=results.Stacked.DID.FD.Full[["ATTSeLeung"]]) %>%

rename(Se=weights)

}

results.Stacked.DID.FD <- rbind(results.Stacked.DID.FD,ATT.Stacked.DID.FD)

# joining all results

resultsDID.SA <- resultsDID.SA %>%

mutate(Method = "SA")

resultsDID.FD <- resultsDID.FD %>%

mutate(Method = "FD")

results.Stacked.DID.FD <- results.Stacked.DID.FD %>%

mutate(Method = "StackedFD") %>%

select(-Group)

resultsDID <- rbind(resultsDID.SA,resultsDID.FD,results.Stacked.DID.FD)

# return results

return(resultsDID)

}

# test

# periods of estimation

tau.test <- c(-19:-2,0:20)

# test <- StaggeredDID22(tau=-19,y='Y',D='Dsunab',d=20,dprime=99,tauprime=1,t="Period",i="id",data=data)

# test <- map_dfr(tau.test,StaggeredDID22,y='Y',D='Dsunab',d=20,dprime=99,tauprime=1,t="Period",i="id",data=data)

testdata <- Outcome.Sample.DID.Long(seed=1,N=1000,K=40,k=20,param=param.basic,rho=0)

testdataTemporal <- Outcome.Sample.DID.Long(seed=1,N=1000,K=40,k=20,param=param.basic,rho=0,cluster='Temporal')Let us now parallelize this function and apply it for several values of \(\rho\).

# programming to run in parallel

# Nsim: number of simulations

# N: number of units in the panel

# K: number of periods in the panel

# k: treatment date

# param: basic parameters

# rho: value of rho

# cluster: whether we cluster or not our treatment effect estimates for temporal autocorrelation ("None", vs "Temporal")

sf.Cluster.MonteCarlo.DID <- function(Nsim,N,K,k,param,rho,cluster='None',ncpus=8){

sfInit(parallel=TRUE,cpus=ncpus)

sfLibrary(tidyverse)

sfLibrary(fixest)

sfLibrary(mvtnorm)

sfLibrary(recipes)

sfLibrary(Matrix)

sfExport('StaggeredDID22')

sfExport('StackedDIDFD')

sim <- sfLapply(1:Nsim,Outcome.Sample.DID.Long,N=N,K=K,k=k,param=param,rho=rho,cluster=cluster)

sfStop()

# generate mean and standard error

sim <- sim %>%

bind_rows(.) %>%

group_by(TimeToTreatment,Method) %>%

summarize(

TE = mean(Coef),

SdTE = sd(Coef),

MeanSeTE = mean(Se)

) %>%

ungroup(.) %>%

mutate(

Rho = rho

)

return(sim)

}

# testing

Nsim <- 10

#sf.test.Cluster.MonteCarlo.DID <- sf.Cluster.MonteCarlo.DID(Nsim=Nsim,N=1000,K=40,k=20,param=param.basic,rho=0)

#sf.test.Cluster.MonteCarlo.DID.temporal <- sf.Cluster.MonteCarlo.DID(Nsim=Nsim,N=1000,K=40,k=20,param=param.basic,rho=0,cluster='Temporal')

# function to compute variance of DID over a grid of rho

# grid.rho: values of rho

# Nsim: number of simulations

# N: number of units in the panel

# K: number of periods in the panel

# k: treatment date

# param: basic parameters

# cluster: whether we cluster or not our treatment effect estimates for temporal autocorrelation ("None", vs "Temporal")

sf.Cluster.MonteCarlo.DID.Grid <- function(grid.rho,Nsim,N,K,k,param,cluster='None',ncpus=8){

sf.test.Cluster.MonteCarlo.DID.grid <- lapply(grid.rho,sf.Cluster.MonteCarlo.DID,Nsim=Nsim,N=N,K=K,k=k,param=param,ncpus=ncpus,cluster=cluster) %>%

bind_rows(.)

return(sf.test.Cluster.MonteCarlo.DID.grid)

}

# testing

grid.rho.test <- c(0,0.5,0.9,0.99,1)

#test.grid <- sf.Cluster.MonteCarlo.DID.Grid(grid.rho=grid.rho.test,Nsim=Nsim,N=1000,K=40,k=20,param=param.basic)

#test.grid.temporal <- sf.Cluster.MonteCarlo.DID.Grid(grid.rho=grid.rho.test,Nsim=Nsim,N=1000,K=40,k=20,param=param.basic,cluster='Temporal')

# true simulations

Nsim <- 1000

sf.simuls.Cluster.DID.grid.rho <- sf.Cluster.MonteCarlo.DID.Grid(grid.rho=grid.rho.test,Nsim=Nsim,N=1000,K=40,k=20,param=param.basic,ncpus=8)Let us now plot the resulting estimates:

# prepapring data

sf.simuls.Cluster.DID.grid.rho <- sf.simuls.Cluster.DID.grid.rho %>%

mutate(

TimeToTreatment = case_when(

TimeToTreatment == "99" ~ 21,

TRUE ~ TimeToTreatment

),

Rho = factor(Rho,levels=as.character(grid.rho.test))

) %>%

pivot_longer(cols=SdTE:MeanSeTE,names_to = "Type",values_to="SeEstim") %>%

mutate(

Type = case_when(

Type == "MeanSeTE" ~ "Estimated",

Type == "SdTE" ~ "Truth",

TRUE ~ ""

),

Type = factor(Type,levels=c("Truth","Estimated"))

) #%>%

#pivot_wider(names_from = "Method",values_from = c('TE','SeEstim'))

ggplot(sf.simuls.Cluster.DID.grid.rho %>% filter(Rho==0),aes(x=TimeToTreatment,y=TE,group=Type,color=Type))+

# geom_pointrange(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim),position=position_dodge(1))+

geom_point(color='red') +

geom_errorbar(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim,color=Type,group=Type),position=position_dodge(1),width=0.5)+

coord_cartesian(ylim=c(-0.15,0.15))+

scale_color_discrete(name='Rho=0')+

theme_bw()+

facet_grid(Method~.)

ggplot(sf.simuls.Cluster.DID.grid.rho %>% filter(Rho==0.5),aes(x=TimeToTreatment,y=TE,group=Type,color=Type))+

# geom_pointrange(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim),position=position_dodge(1))+

geom_point(color='red') +

geom_errorbar(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim,color=Type,group=Type),position=position_dodge(1),width=0.5)+

coord_cartesian(ylim=c(-0.15,0.15))+

scale_color_discrete(name='Rho=0.5')+

theme_bw()+

facet_grid(Method~.)

ggplot(sf.simuls.Cluster.DID.grid.rho %>% filter(Rho==0.9),aes(x=TimeToTreatment,y=TE,group=Type,color=Type))+

# geom_pointrange(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim),position=position_dodge(1))+

geom_point(color='red') +

geom_errorbar(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim,color=Type,group=Type),position=position_dodge(1),width=0.5)+

coord_cartesian(ylim=c(-0.15,0.15))+

scale_color_discrete(name='Rho=0.9')+

theme_bw()+

facet_grid(Method~.)

ggplot(sf.simuls.Cluster.DID.grid.rho %>% filter(Rho==0.99),aes(x=TimeToTreatment,y=TE,group=Type,color=Type))+

# geom_pointrange(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim),position=position_dodge(1))+

geom_point(color='red') +

geom_errorbar(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim,color=Type,group=Type),position=position_dodge(1),width=0.5)+

coord_cartesian(ylim=c(-0.15,0.15))+

scale_color_discrete(name='Rho=0.99')+

theme_bw()+

facet_grid(Method~.)

ggplot(sf.simuls.Cluster.DID.grid.rho %>% filter(Rho==1),aes(x=TimeToTreatment,y=TE,group=Type,color=Type))+

# geom_pointrange(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim),position=position_dodge(1))+

geom_point(color='red') +

geom_errorbar(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim,color=Type,group=Type),position=position_dodge(1),width=0.5)+

coord_cartesian(ylim=c(-0.15,0.15))+

scale_color_discrete(name='Rho=1')+

theme_bw()+

facet_grid(Method~.)

# ggplot(sf.simuls.Cluster.DID.grid.rho,aes(x=TimeToTreatment,y=TE_FD,group=Type,color=Type))+

# # geom_pointrange(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim),position=position_dodge(1))+

# geom_point(color='red') +

# geom_errorbar(aes(ymin=TE_FD-1.96*SeEstim_FD,ymax=TE_FD+1.96*SeEstim_FD,color=Type,group=Type),position=position_dodge(1),width=0.2)+

# geom_errorbar(aes(ymin=TE_SA-1.96*SeEstim_SA,ymax=TE_SA+1.96*SeEstim_SA,color=Type,group=Type),position=position_dodge(1),width=0.5)+

# geom_errorbar(aes(ymin=TE_StackedFD-1.96*SeEstim_StackedFD,ymax=TE_StackedFD+1.96*SeEstim_StackedFD,color=Type,group=Type),position=position_dodge(1),width=0.9)+

# theme_bw()+

# facet_grid(Rho~.)

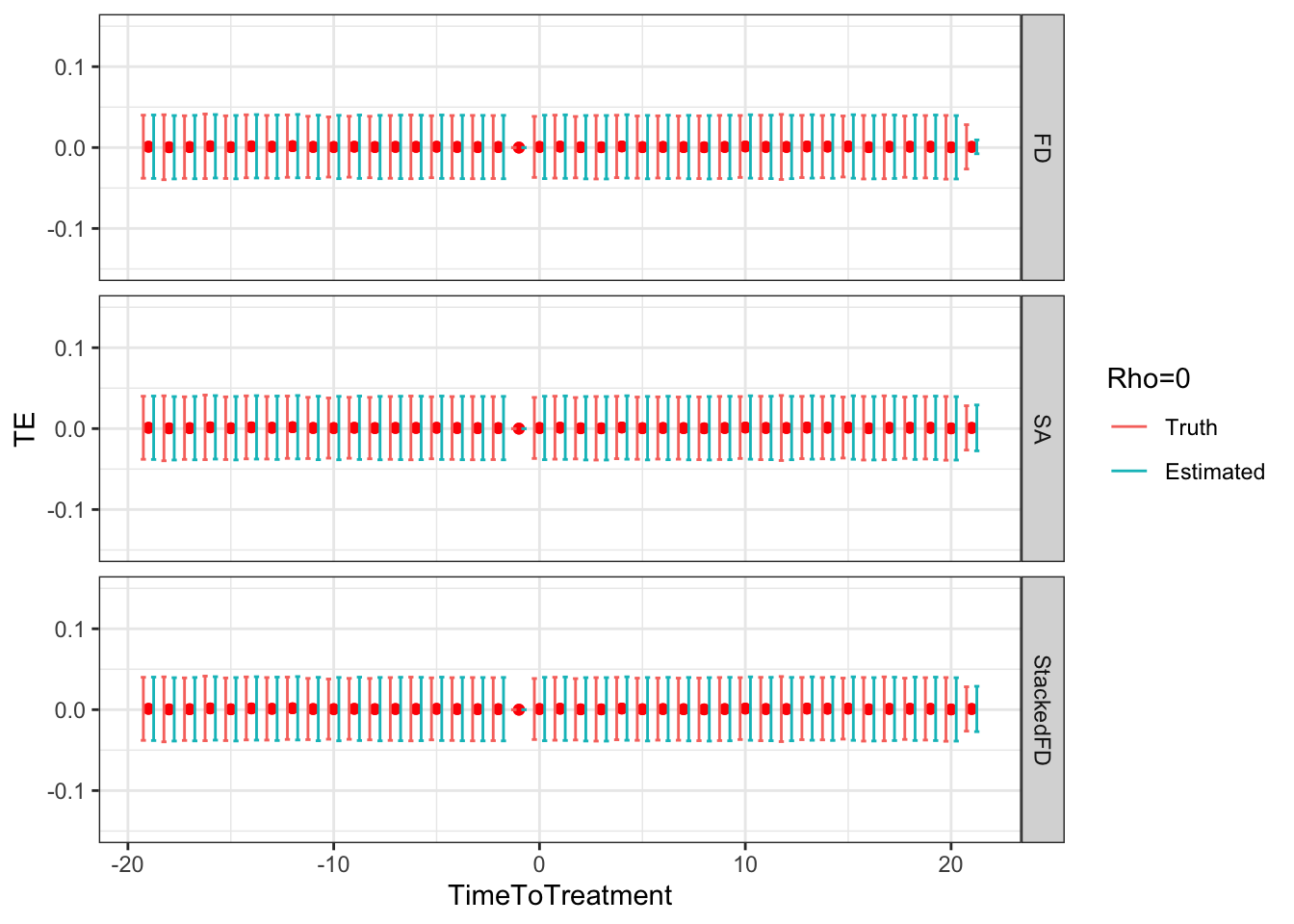

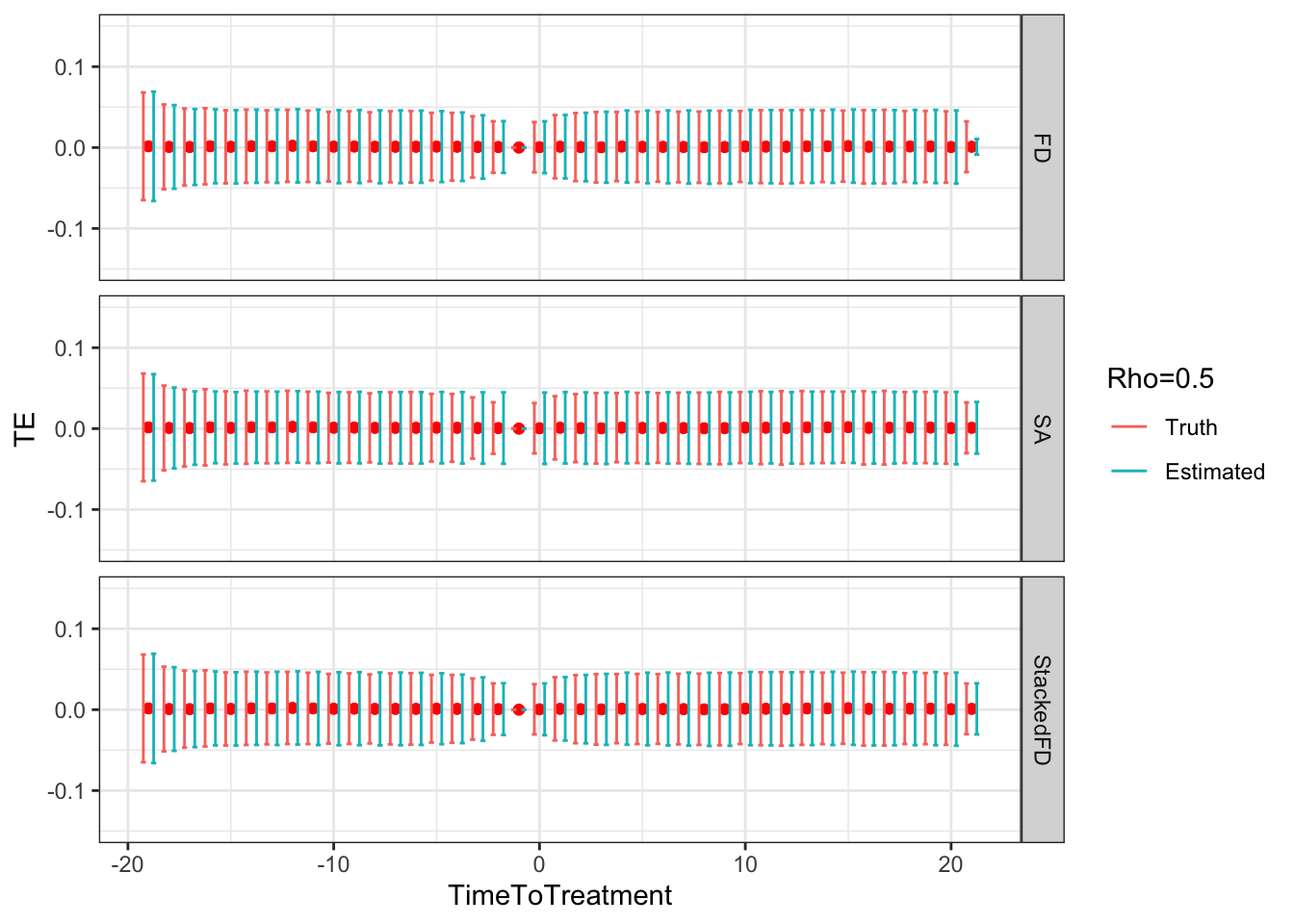

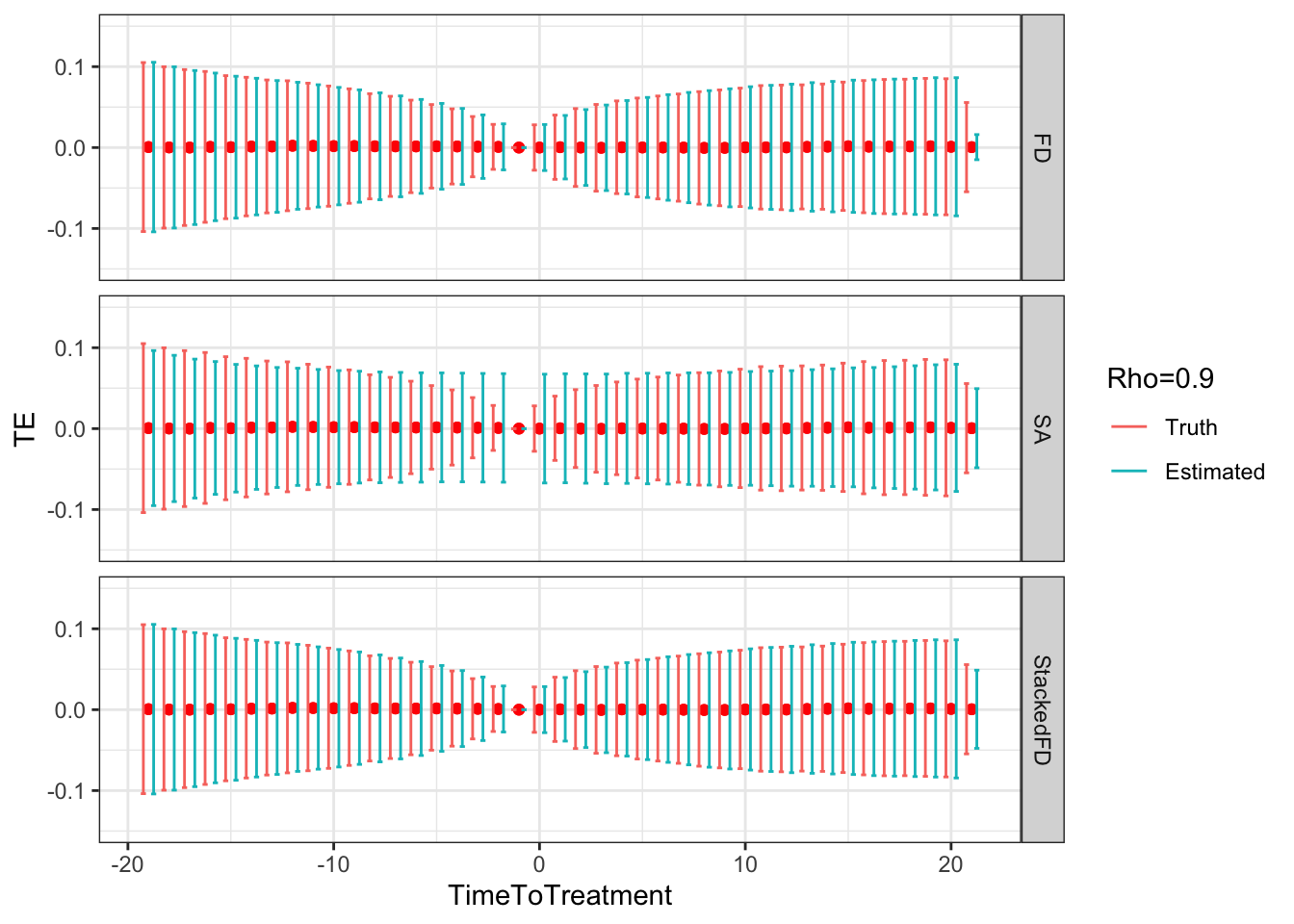

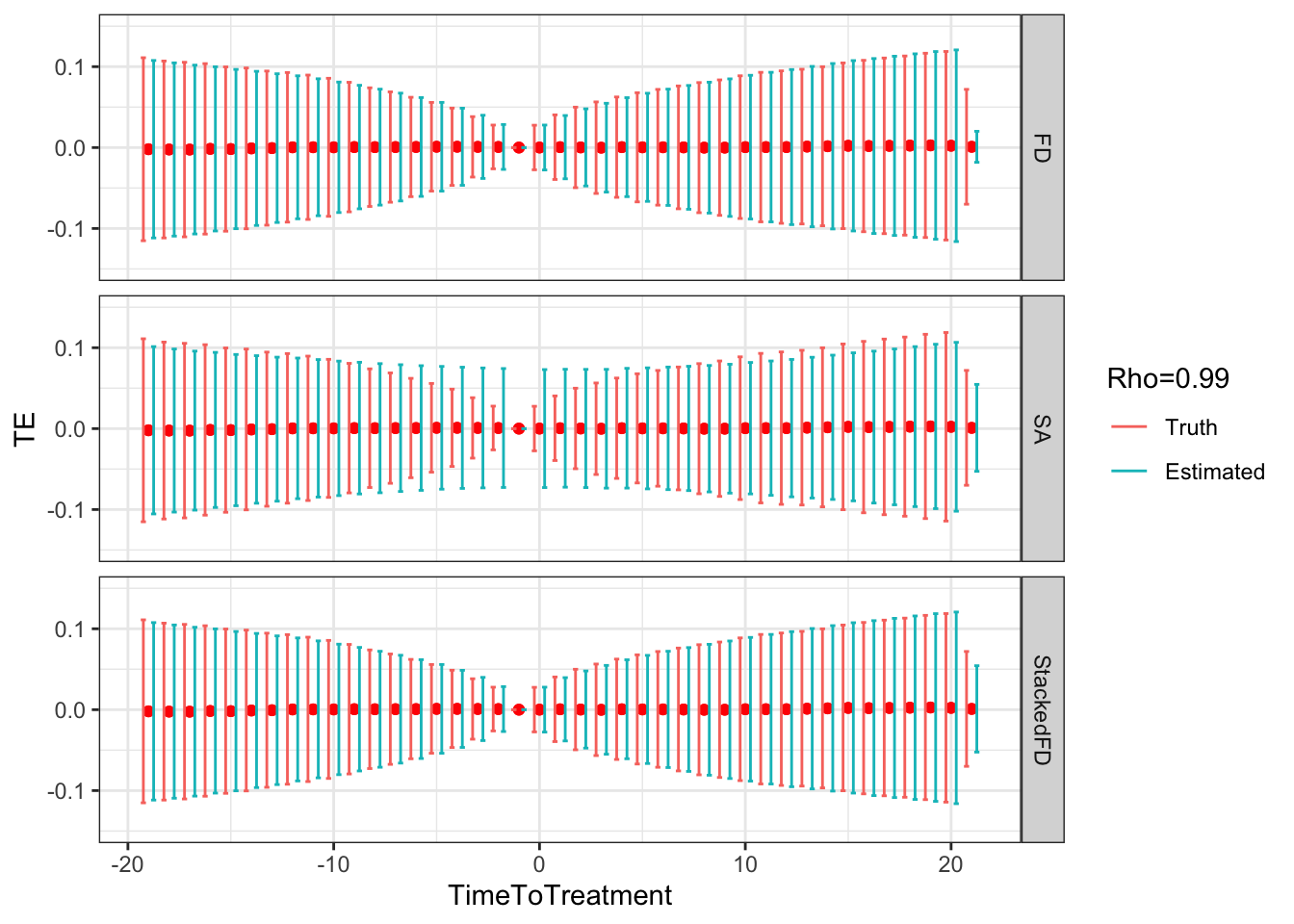

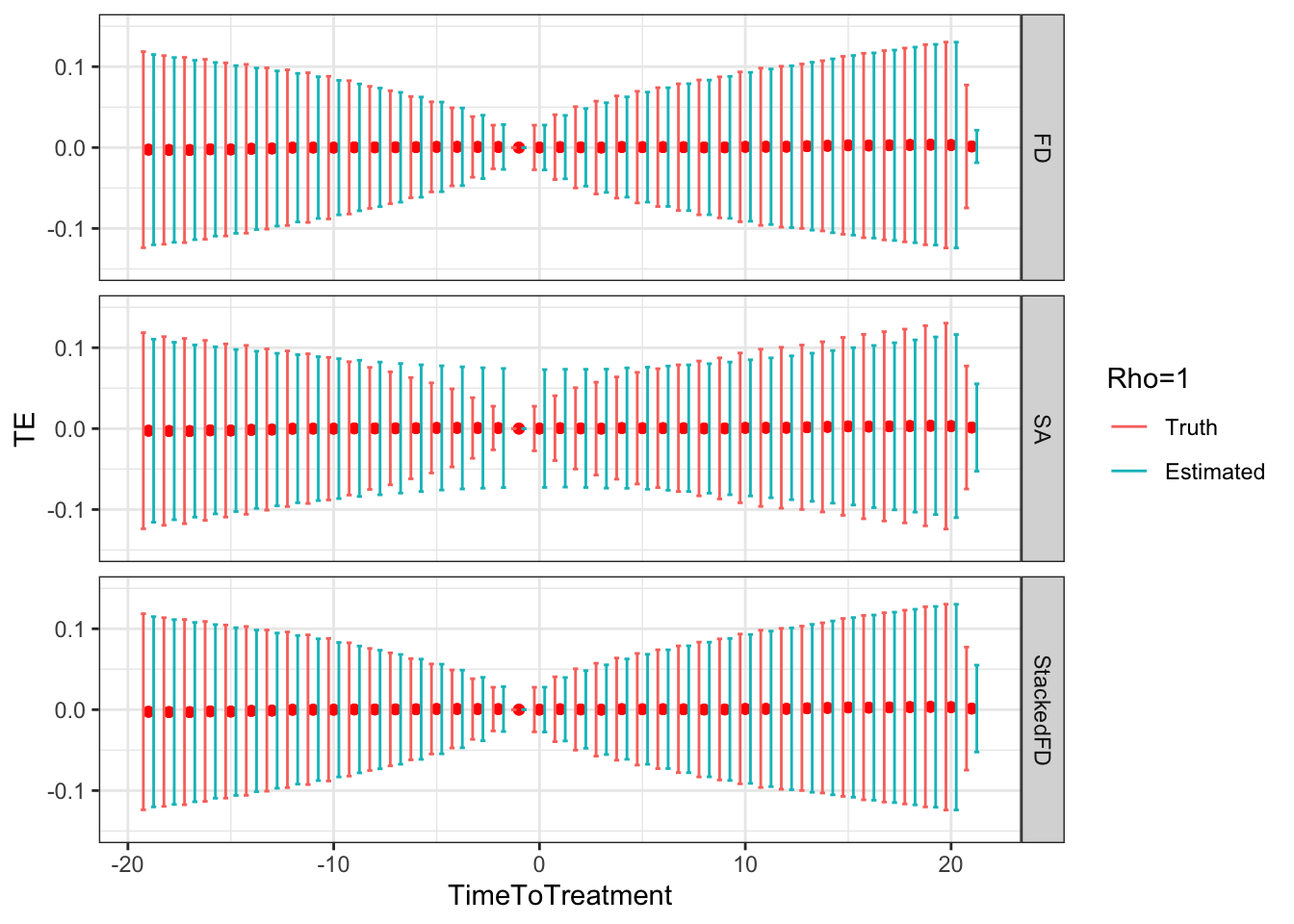

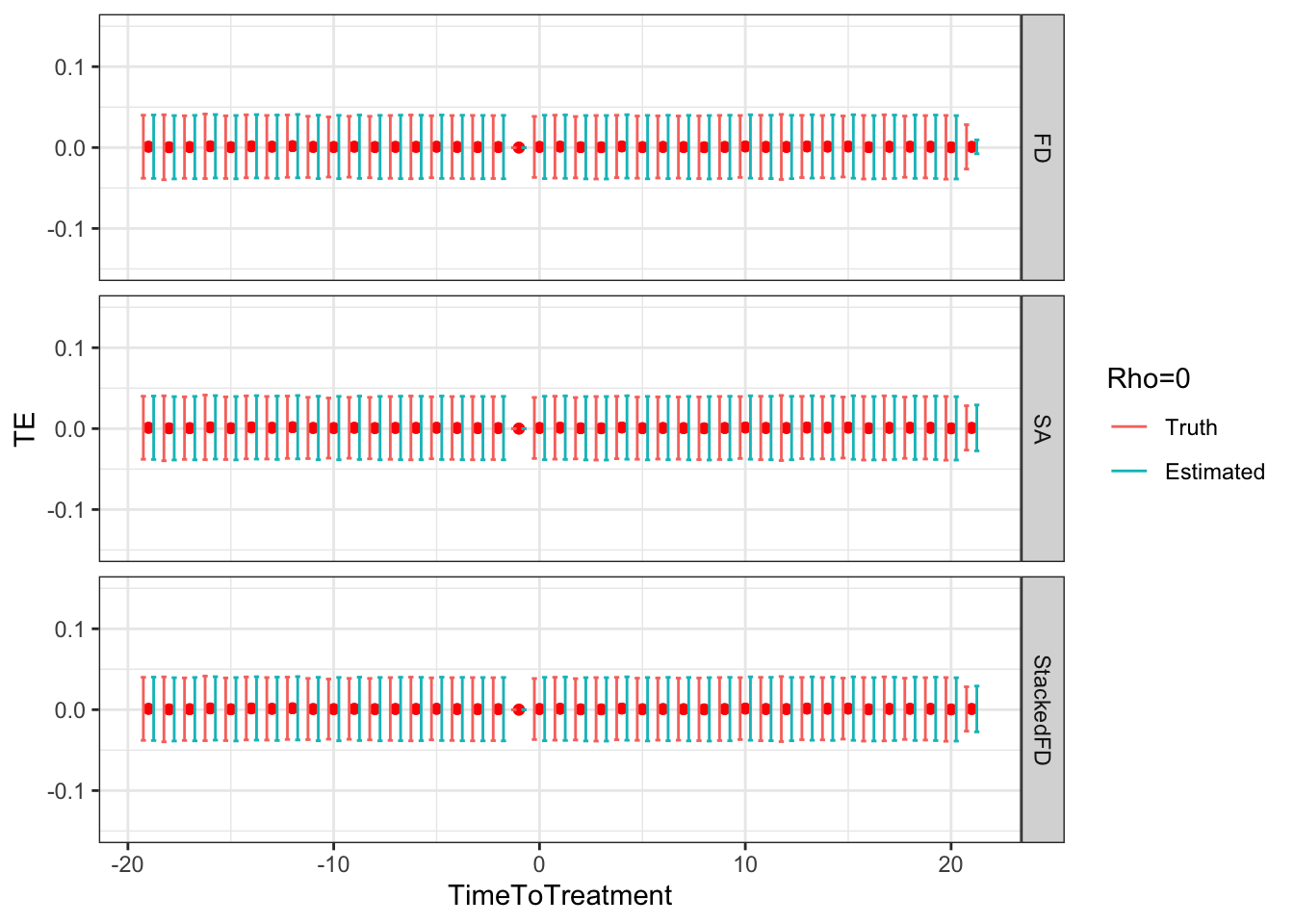

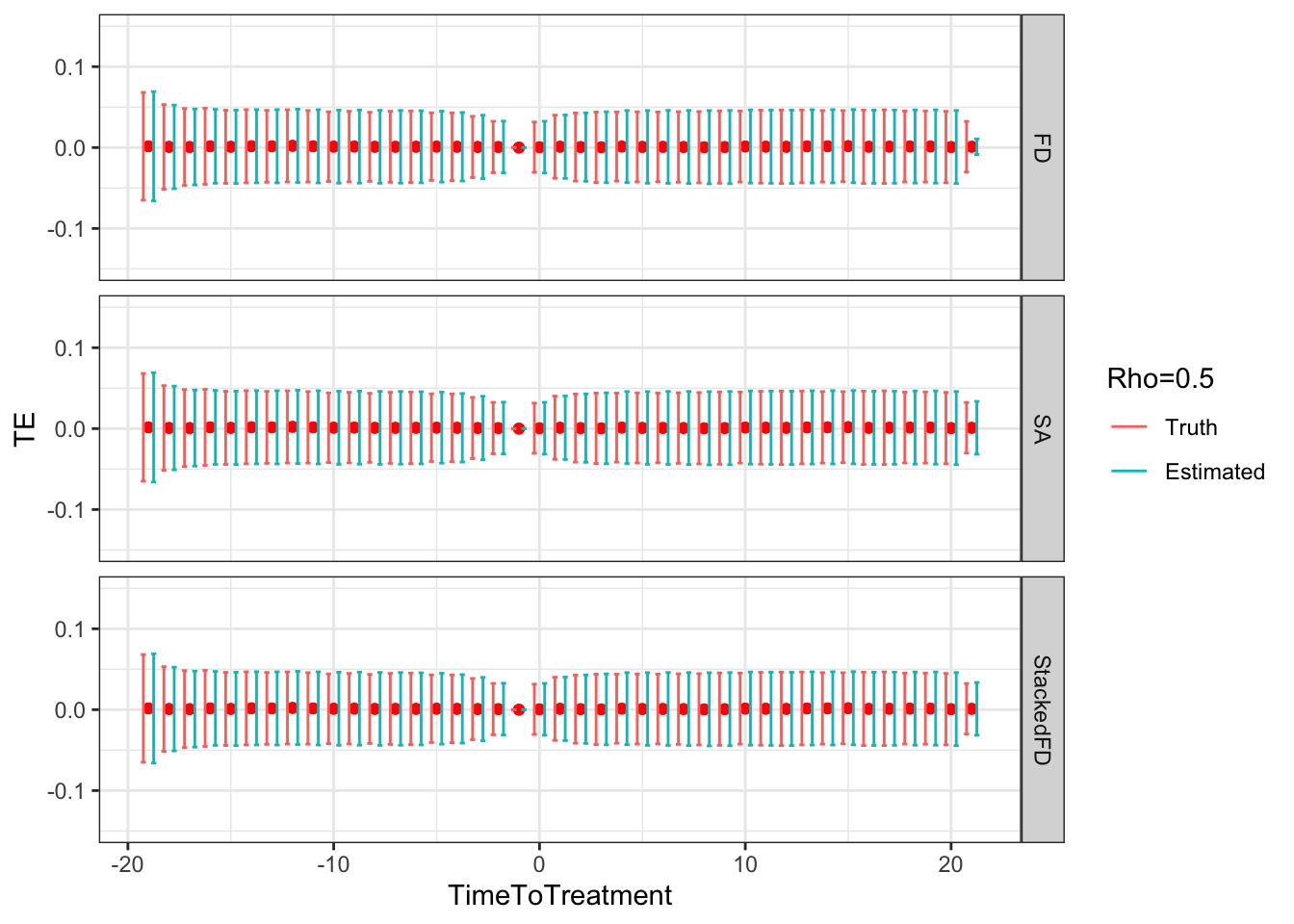

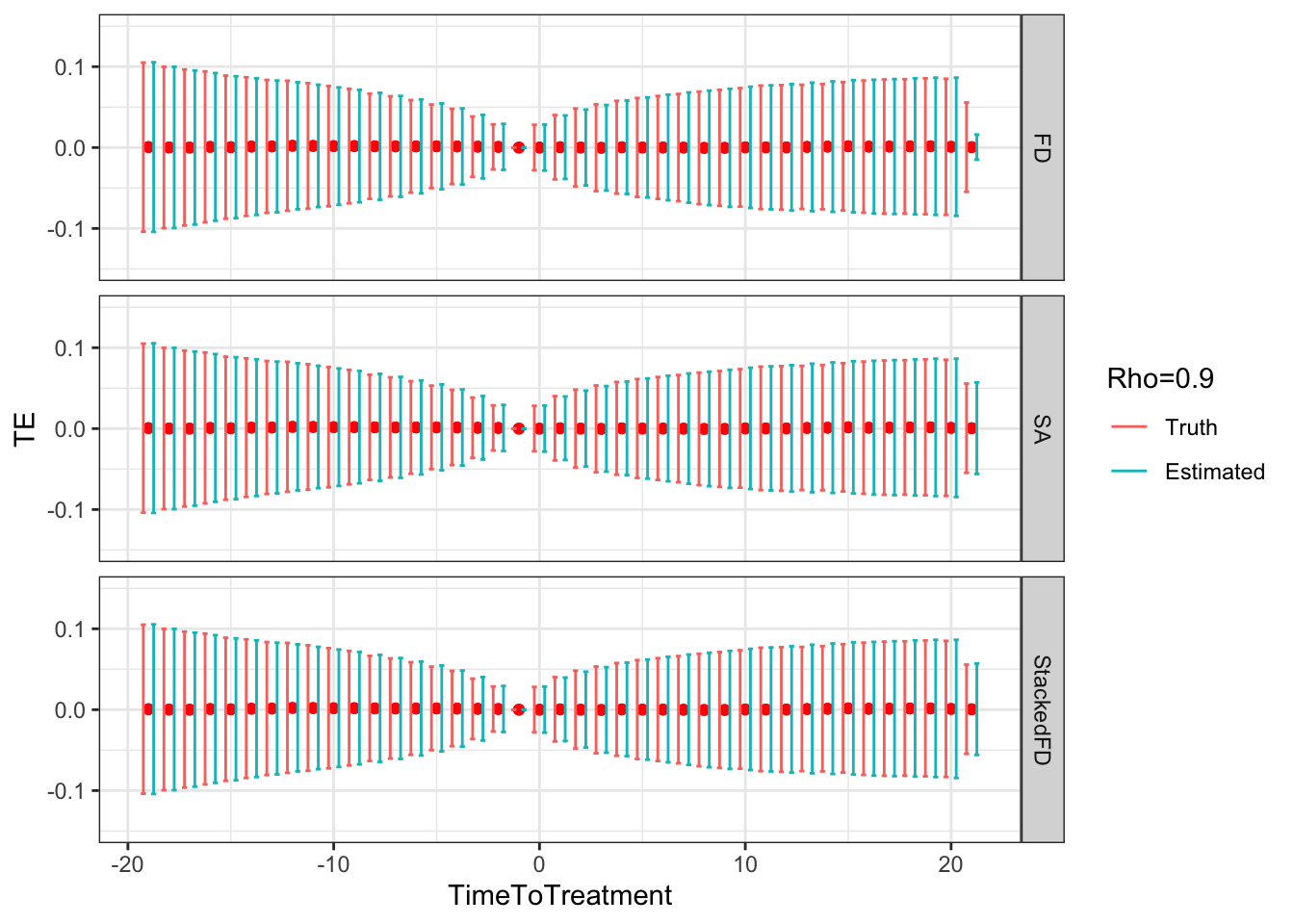

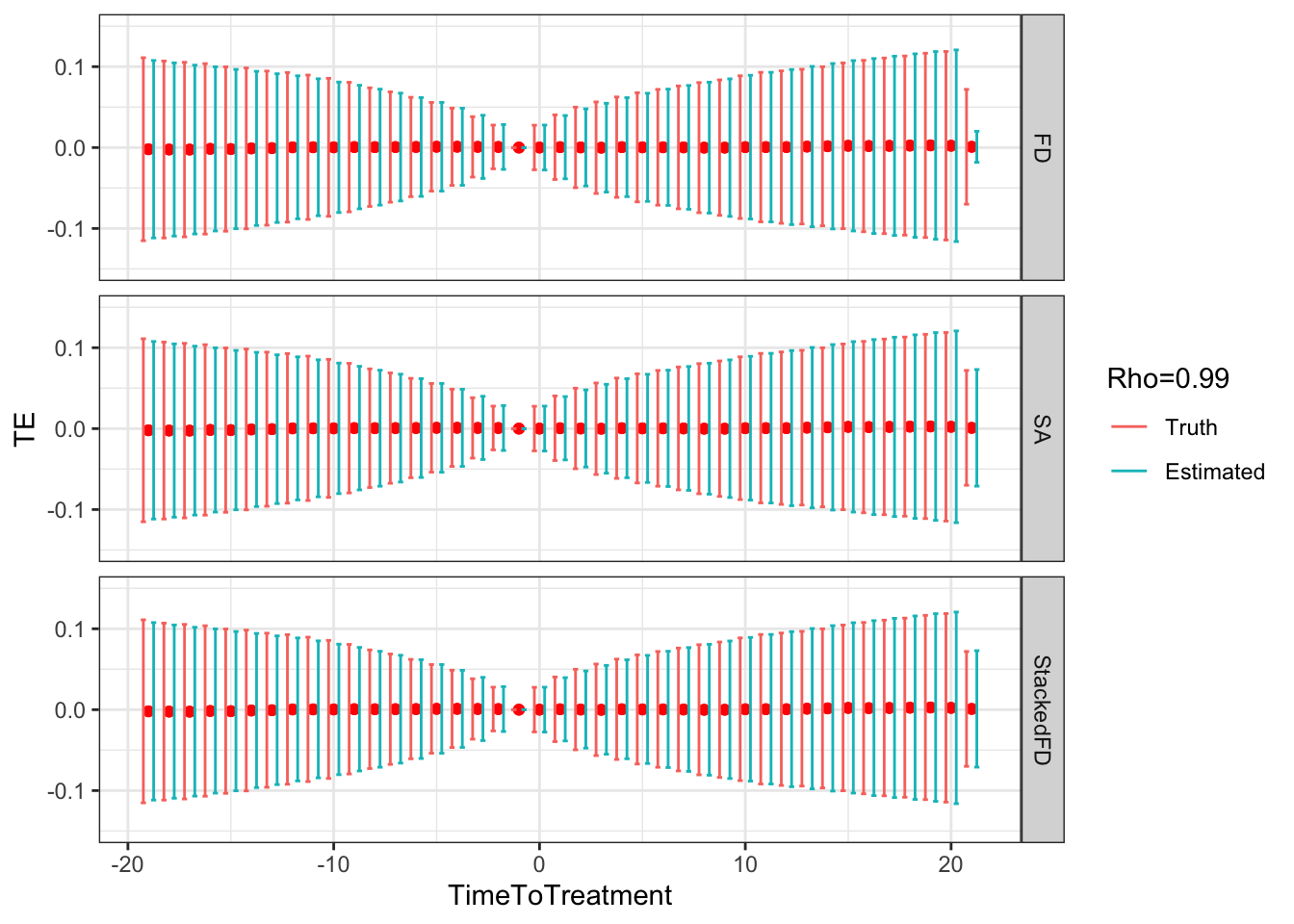

Figure 9.5: DID estimates with increasing temporal autocorrelation in outcomes

Figure 9.5 shows that indeed sampling noise increases with autocorrelation in panel data. For the same sample size of \(N=1000\), the true 99% sampling noise for the average effect of the treatment on the treated estimated by Monte Carlo simulations is equal to:

- 0.07 when \(\rho=0\),

- 0.08 when \(\rho=0.5\),

- 0.14 when \(\rho=0.9\),

- 0.19 when \(\rho=0.99\),

- 0.2 when \(\rho=1\).

The heteroskedasticity-robust estimates of 99% sampling noise for the average effect of the treatment on the treated ignoring autocorrelation are equal to (taking the average estimate of sampling noise over Monte Carlo replications for the the fixest implementation of the Sun and Abraham estimator and for the Stacked First Difference estimator, respectively):

- 0.07 and 0.07 when \(\rho=0\),

- 0.08 and 0.08 when \(\rho=0.5\),

- 0.13 and 0.13 when \(\rho=0.9\),

- 0.14 and 0.14 when \(\rho=0.99\),

- 0.14 and 0.14 when \(\rho=1\).

This means that heteroskedasticity-robust estimates of 99% sampling noise for the average effect of the treatment on the treated ignoring autocorrelation is smaller than the truth, by a factor of (for the the fixest implementation of the Sun and Abraham estimator and for the Stacked First Difference estimator, respectively):

- 1.04 and 1.02 when \(\rho=0\),

- 1.02 and 1.01 when \(\rho=0.5\),

- 0.89 and 0.88 when \(\rho=0.9\),

- 0.76 and 0.75 when \(\rho=0.99\),

- 0.71 and 0.71 when \(\rho=1\).

As true autocorrelation increases, the heteroskedasticity-robust estimator of the sampling noise of the TT parameter increasingly over-estimates true sampling noise. At the same time, the heteroskedasticity-robust \(2\times 2\) estimates of sampling noise underestimate the sampling noise of ATT in a major way. This is because they for now ignore any autocorrelation between \(2\times 2\) estimates as studied in Theorem 4.27.

Remark. An interesting feature of Figure 9.5 is that, when \(\rho>0\), sampling noise decreases as we move closer to to the treatment date and increases as we move away.

Why is that so?

It is due to a combination of our choice of reference period and of the extent of autocorrelation in the error terms.

Indeed, following Theorem 4.25, we know that the sampling noise of each individual \(2\times 2\) estimate depends on the variance of \(Y^0_{i,d+\tau}-Y^0_{i,d-1}\), and thus on the variance of \(U_{i,d+\tau}-U_{i,d-1}\)

Under our \(AR(1)\) model of dynamics of \(U_{i,t}\) and substituting iteratively, we have:

\[\begin{align*} U_{i,d+\tau}-U_{i,d-1} & = \rho^{\tau+1}U_{i,d-1}+\sum_{k=0}^{\tau}\rho^{k}\epsilon_{i,d+\tau-k}-U_{i,d-1}. \end{align*}\]

As a consequence, we have:

\[\begin{align*} \var{U_{i,d+\tau}-U_{i,d-1}} & = (1-\rho^{\tau+1})^2\var{U_{i,d-1}}+\sum_{k=0}^{\tau}\rho^{2k}\sigma^2_{\epsilon}\\ & = (1-\rho^{\tau+1})^2\var{U_{i,d-1}}+\frac{1-\rho^{2(\tau+1)}}{1-\rho^{2}}\sigma^2_{\epsilon}, \end{align*}\]

where the last term in the right hand side of the second equality is valid when \(\rho<1\), and is replaced by \((\tau+1)\sigma^2_{\epsilon}\) when \(\rho=1\). That formula means that when \(\tau\) is close to \(-1\), that is when the estimation period is close to the reference period, the variance of the \(2\times 2\) DID estimate is small. When \(\tau\) increases and the estimation period gets further away from the reference period, the variance of the \(2\times 2\) DID estimate increases. The intuition for this result is that, with autocorrelated error terms, the outcomes of the same individual observed at periods that are close to each other in time are positively correlated, and the first differencing of DID gets rid of part of their influence. In the limit, with perfectly persistent error terms (\(\rho=1\)), the shocks that occur up to the reference period \(d-1\) are completely cancelled (first part of the right hand side of the equation).

Remark. A more unexpected result, is that, when autocorrelation increases, fixest heteroskedasticity-robust estimates of sampling noise using Sun and Abraham estimator overestimate true sampling noise in a major way when treatment and reference periods are close to each other (Method=="SA"), and seems to slighlty underestimate it when the treatment and reference period are far apart.

This is strange because using heteroskedasticity-robust \(2\times 2\) and Stacked First Difference estimates of sampling noise gives a correct estimate of the amount of true sampling noise, irrespective of the level of autocorrelation in the data.

It looks as if the heteroskedasticity-robust estimator of sampling noise in fixest fails at identifying and estimating correctly the heteroskedasticity that takes place across time periods, and instead smooths out the variance over all time periods.

The reason for this behavior lies in how fixest estimates sampling noise.

The feols command in fixest uses a within type of estimator.

As a consequence, it recovers estimates of residuals in levels, not in first difference as with the \(2\times 2\) estimates in First Difference or the Stacked FD estimator.

Therefore, the feols command in fixest does not use the estimator in Theorem 4.25 which involves the residual of the FD estimator, but rather something equivalent to the estimate in Theorem 4.24, with \(Y_{i,t}\) replaced by \(U_{i,t}\).

These two approaches are equivalent when the error terms are independent over time (i.e under Assumption 4.28), but they do not yield the same estimates when the error terms are correlated over time.

Indeed, \(\var{Y_{i,d+\tau}^1-Y_{i,d-1}^0}=\var{Y_{i,d+\tau}^1}+\var{Y_{i,d-1}^0}-2\cov{Y_{i,d+\tau}^1,Y_{i,d-1}^0}\).

When \(\cov{Y_{i,d+\tau}^1,Y_{i,d-1}^0}>0\), the variance of the difference is smaller than the sum of the variances of each components, and thus the estimate of samling noise based on the FD estimators is going to be smaller than the one based on the within estimator (as in fixest).

It is less clear why fixest heteroskedasticity-robust estimates of sampling noise using Sun and Abraham estimator slighlty underestimates sampling noise when the treatment and reference period are far apart.

This is an open question at the time of writing.

9.2.2 Design effect in panel data

Let us now derive an estimate of the design effect in panel data.

9.2.2.1 Design effect for \(2\times 2\) DID estimates

Autocorrelation of error terms over time does not affect the estimates of sampling noise for the individual \(2\times 2\) DID estimates in panel data based on the First-Difference transformation. Indeed, Theorem 4.25 only rests on the fact that outcomes are independent over space, not over time (Assumption 4.15). This is confirmed by the simulations in Figure 9.5: when \(\rho>0\), and thus there is autocorrelation between outcomes over time, the estimates of sampling noise of the individual \(2\times 2\) DID estimates based on Theorem 4.25 (for the \(2\times 2\) First Difference and Stacked First Difference estimators) are correct. The reason is that the \(2\times 2\) First Difference estimators are purely cross-sectional: they do not involve observations from several periods. All of that is taken into account in the differencing part. As a consequence, the validity of the estimates of sampling noise of the \(2\times 2\) DID estimates based on Theorem 4.25 are valid under any type of autocorrelation, which makes them extremely attractive.

In contrast, \(2\times 2\) DID estimates in panel data that are not based on the First Difference transformation, but rather on the within transformation, such as the ones obtained using the feols command of the fixest package, require an absence of temporal autocorrelation to be valid.

They will overestimate the extent of sampling noise when error terms are positively correlated over time, and they will underestimate sampling noise when error terms are negatively correlated over time.

9.2.2.2 Design effect for the Average Treatment Effect on the Treated

Estimates of sampling noise for the Average Treatment Effect on the Treated will always be affected by temporal auto-correlation of the error terms, even when the estimates of sampling noise for the individual \(2\times 2\) DID estimates is not. The intuition for why is that, when error terms are correlated over time, individual \(2\times 2\) DID estimates are more correlated with each other than what Theorem 4.27 would suggest. If they are more correlated, then the variance of their weighted average increases, since it is more likely that two individual \(2\times 2\) DID estimates look alike than what we would have expected under Assumption 4.28. Let’s see how the sampling noise of the Average Treatment Effect on the Treated changes when relaxing Assumption 4.28.

Hypothesis 9.2 (AR(1) autocorrelation and i.i.d. sampling in panel data) We assume that potential outcomes are generated as follows:

\[\begin{align*} Y^0_{i,t} & = \mu_i + \delta_t + U^0_{i,t}\\ Y^1_{i,t} & = \mu_i + \delta_t + \bar{\alpha} +\eta_{i,t} + U^0_{i,t}\\ U^0_{i,t} & = \rho U^0_{i,t-1} + \epsilon_{i,t}, \end{align*}\]

with \(\esp{U^0_{i,t}}=\esp{\eta_{i,t}}=0\), \(\forall t\), \(\esp{U^0_{i,t}|D_i}=0\), \(\forall t\) and:

\[\begin{align*} \forall i,j\leq N\text{, }\forall t,t'\leq T\text{, with either }i\neq j \text{ or } t\neq t' & (\epsilon_{i,t},\eta_{i,t},D_i)\Ind(\epsilon_{j,t'},\eta_{j,t'},D_j),\\ & (\epsilon_{i,t},\eta_{i,t},D_i)\&(\epsilon_{j,t'},\eta_{j,t'},D_j)\sim F_{\epsilon,\eta,D}. \end{align*}\]

We also assume that \(U^0_{i,t}\Ind\epsilon_{j,t'},\eta_{j,t'}\), \(\forall i,j\leq N\text{, }\forall t,t'\leq T\).

Remark. Assumption 9.2 is less restrictive than Assumption 4.28: it allows for error terms for the same unit \(i\) to be correlated over time through an AR(1) process. Assumption 9.2 nevertheless still imposes than treatment effects are not autocorrelated over time, which is still pretty restrictive.

Theorem 9.2 (Asymptotic Distribution of Treatment of the Treated Estimated Using Sun and Abraham Estimator in Panel Data with AR(1) Error Terms) Under Assumptions 4.12, 4.13, 4.14, 9.2 and 4.16, and with panel data containing a total of \(N\) units observed over \(T\) time periods, we have:

\[\begin{align*} \sqrt{N}(\hat\Delta^{Y}_{TT_{SA}}(k)-\Delta^{Y}_{TT_{SA}}(k)) & \stackrel{d}{\rightarrow} \mathcal{N}\left(0,\sum_d\sum_{\tau}V_P(\hat\beta^{SA}_{d,\tau})(w^k(d,d-1,\tau,\infty))^2\right.\\ & \phantom{\stackrel{d}{\rightarrow}}\left.+\sum_{d}\sum_{d'}\sum_{\tau}\sum_{\tau'\neq\tau} \text{Cov}_P(\hat\beta^{SA}_{d,\tau},\hat\beta^{SA}_{d',\tau'})w^k(d,d-1,\tau,\infty)w^k(d',d'-1,\tau',\infty)\right), \end{align*}\]

where:

\[\begin{align*} V_P(\hat\beta^{SA}_{d,\tau}) & =\frac{1}{p^{d,\infty}}\left(\frac{\var{Y_{i,d+\tau}^1-Y_{i,d-1}^0|D_i=d}}{p^{d,\infty}_D}+\frac{\var{Y_{i,d+\tau}^0-Y_{i,d-1}^0|D_i=\infty}}{1-p^{d,\infty}_D}\right)\\ \text{Cov}_P(\hat\beta^{SA}_{d,\tau},\hat\beta^{SA}_{d',\tau'}) & =\frac{1}{p^{d,\infty}}\left[\frac{\esp{\Delta\epsilon^{d,\tau}_i\Delta\epsilon^{d',\tau'}_i|D_i=\infty}}{1-p^{d,\infty}_D}+\frac{\esp{\Delta\epsilon^{d,\tau}_i\Delta\epsilon^{d',\tau'}_i|D_i=d}}{p^{d,\infty}_D}\right] \text{ when } d=d'\\ & = \frac{\esp{\Delta\epsilon^{d,\tau}_i\Delta\epsilon^{d',\tau'}_i|D_i=d}}{p^{d',\infty}(1-p^{d',\infty}_D)} \text{ when } d\neq d', \end{align*}\]

with \(p^{d,\infty}=\Pr(D_i=d\cup D_i=\infty)\) and \(p^{d,\infty}_D=\Pr(D_i=d|D_i=d\cup D_i=\infty)\).

Proof. See Section A.5.2.

9.2.3 Estimating sampling noise in panel data with autocorrelated error terms

We are now equipped to estimate sampling noise in panel data with autocorrelated error terms. As in the case of spatial autocorrelation, the solutions involve using the plug-in estimator based on Theorem 9.2, using cluster-robust standard errors, using Feasible Generalized Least Squares, the bootstrap and randomization inference.

9.2.3.1 Using the plug-in estimator

Although a little bit tedious, it is possible to estimate each component of the plug-in formula in Theorem 9.2, whose details can be found in Section A.5.2. We need mostly to estimate \(\rho\), by regressing \(\hat{U}^0_{i,t}\) on \(\hat{U}^0_{i,t-1}\). We then need to estimate the variance terms. This is left as an exercise.

9.2.3.2 Using Feasible Generalized Least Squares

It is possible to build the matrix \(\hat{\Omega}_{GLS}=\hatesp{UU'|X}\) under Assumption 4.28. It is a block diagonal matrix, with all blocks being the observations over time of the same unit in the panel. The covariance terms depend on \(\hat\rho\) and the variance of \(\hat{U}^0_{i,t}\) and \(\eta_{i,t}\). Estimating the terms in this matrix is left as an exercise. CLuster-robust FGLS estimates are also feasible, obviously.

9.2.3.3 Using Cluster-Robust Standard Errors

As in the spatial clustering case, it is possible to use a cluster robust covariance matrix in panel data with autocorrelated error terms.

For the within estimator, the formula can be derived in the same way, except with clusters being the groups of observations belonging to the same unit observed over time.

Estimating this formula can be done with either the sandwich package or the cluster option in the fixest package.

Here, I want to introduce an alternative approach, which is going to make our lives much easier when correlation between error terms is going to be richer and more complex. This approach is due to Leung (2020) and it generalizes cluster-robust covariance matrices to a much broader set of cases while retaining the interpretability of the cluster-robust standard errors. Leung’s estimator of the variance of the OLS estimator is as follows: \(\hatvar{\hat{\Theta}_{OLS,Leung}}=(X'X)^{-1}\hat{\mathcal{M}}'G\hat{\mathcal{M}}(X'X)^{-1}\), where \(\hat{\mathcal{M}}=(X_1\hat{\epsilon}_1,\dots,X_N\hat{\epsilon}_N)'\), with \(\hat{\epsilon}\) the vector of regression residuals and \(X_k\) the vector of covariates for observation \(k\), and \(G\) is a matrix indicating which observations are correlated with each other. In the case of temporal autocorrelation, \(G_{i,j}\) takes value \(1\) when observations \(i\) and \(j\) in the dataset belong to the same unit and zero otherwise.

Example 9.8 Let’s see how this all works in our example.

We actually already introduced the cluster option in the original Monte Carlo simulation functions.

Extending our simulations to clustering is therefore straightfoward.

# true simulations

Nsim <- 1000

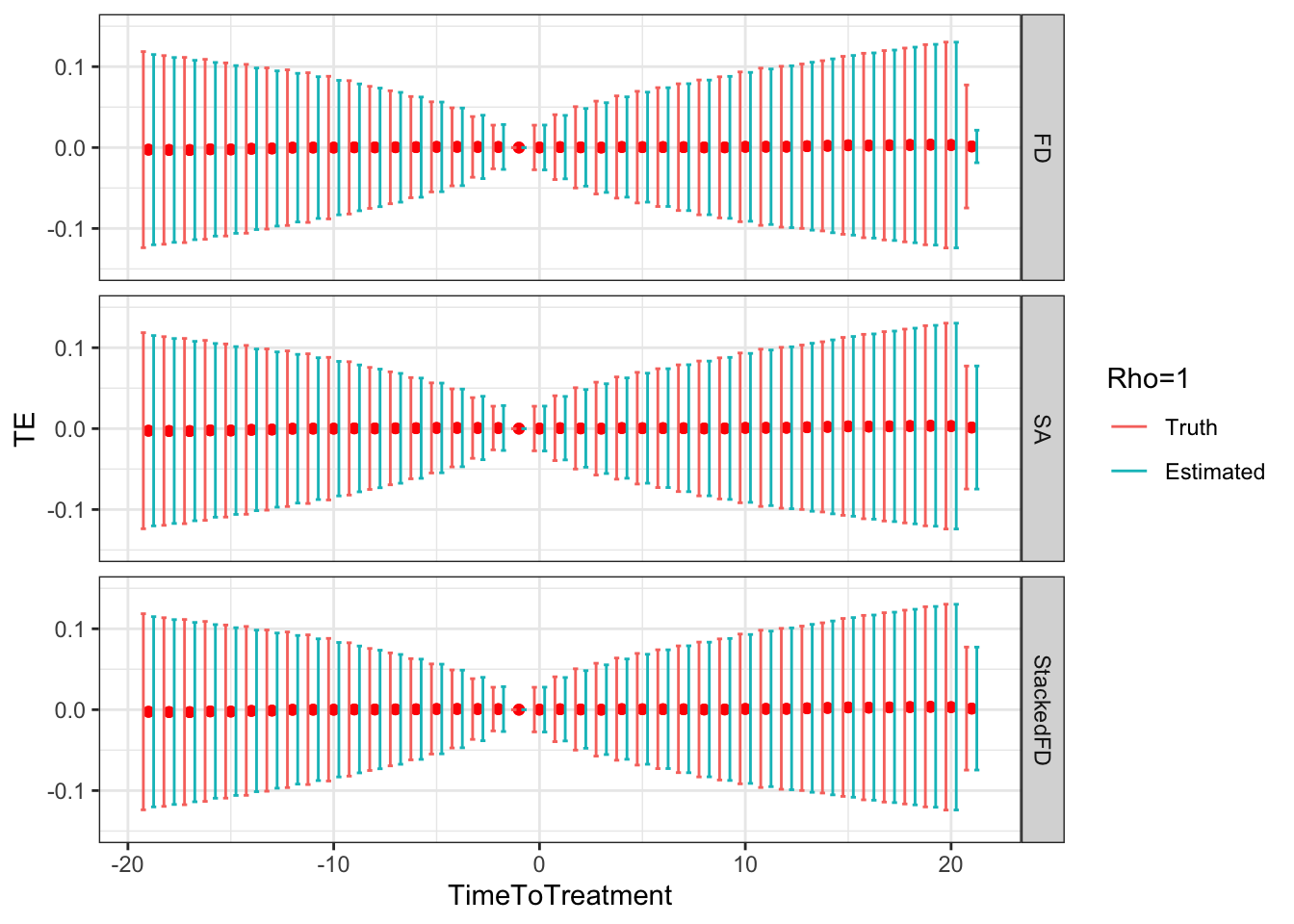

sf.simuls.Cluster.DID.Temporal.grid.rho <- sf.Cluster.MonteCarlo.DID.Grid(grid.rho=grid.rho.test,Nsim=Nsim,N=1000,K=40,k=20,param=param.basic,cluster='Temporal',ncpus=8)Let us now plot the resulting estimates:

# prepapring data

sf.simuls.Cluster.DID.Temporal.grid.rho <- sf.simuls.Cluster.DID.Temporal.grid.rho %>%

mutate(

TimeToTreatment = case_when(

TimeToTreatment == "99" ~ 21,

TRUE ~ TimeToTreatment

),

Rho = factor(Rho,levels=as.character(grid.rho.test))

) %>%

pivot_longer(cols=SdTE:MeanSeTE,names_to = "Type",values_to="SeEstim") %>%

mutate(

Type = case_when(

Type == "MeanSeTE" ~ "Estimated",

Type == "SdTE" ~ "Truth",

TRUE ~ ""

),

Type = factor(Type,levels=c("Truth","Estimated"))

) #%>%

#pivot_wider(names_from = "Method",values_from = c('TE','SeEstim'))

ggplot(sf.simuls.Cluster.DID.Temporal.grid.rho %>% filter(Rho==0),aes(x=TimeToTreatment,y=TE,group=Type,color=Type))+

# geom_pointrange(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim),position=position_dodge(1))+

geom_point(color='red') +

geom_errorbar(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim,color=Type,group=Type),position=position_dodge(1),width=0.5)+

coord_cartesian(ylim=c(-0.15,0.15))+

scale_color_discrete(name='Rho=0')+

theme_bw()+

facet_grid(Method~.)

ggplot(sf.simuls.Cluster.DID.Temporal.grid.rho %>% filter(Rho==0.5),aes(x=TimeToTreatment,y=TE,group=Type,color=Type))+

# geom_pointrange(aes(ymin=TE-1.96*SeEstim,ymax=TE+1.96*SeEstim),position=position_dodge(1))+

geom_point(color='red') +